It can be agonizing to watch your portfolio decline during a down market. Our human nature is to react erratically, which can be destructive to your financial plan. While it is important to stay the course, that doesn't mean you need to be idle. There is always an opportunity to do something to better your financial house. Here are a few productive things you can do as an investor during a down market:

Do:

Take Advantage of Opportunity

Invest cash: Risk assets like stocks are discounted, and as such, now may be a timely opportunity to invest the cash you have on the sidelines. Yes, markets may go down further, so be prepared for additional short-term losses. When investing additional dollars, don't let a desire to time the market-bottom perfectly get in the way of taking advantage of the opportunity.

Look for opportunities to Tax-loss harvest: Tax-loss harvesting allows you to get a tax break for poor-performing investments in a brokerage account. This strategy allows a taxpayer to offset other taxable gains and potentially claim a deduction against ordinary income. This is an unseen benefit for investors who have a brokerage account and want to use poor-performing investments to lessen their tax burden. (See Tax Tips in a Down Market)

Keep an Eye on your Financial Goals

Rebalance: Market moves can result in a drift of your account's investments. Rebalancing your investments to your desired investment strategy can restore the appropriate level of risk and return to your account. Making sure you have an appropriate amount in stocks will help you take advantage of the possible market rebound.

Accelerate Savings: Are you systematically saving into an investment account, such as a 401(k), IRA, or brokerage account? Consider making a larger contribution now to take advantage of the opportunity. This is a similar thought process to investing cash.

Roth IRA conversions: Stock market downturns make for an opportunity to convert traditional IRA dollars to a Roth. When you convert dollars to a Roth IRA, you are responsible to pay income tax on the conversion amount. You are trading the tax-deferred (pay taxes when you withdraw) growth for tax-free growth. Before you complete a Roth conversion make sure you understand the tax implications and talk to your advisor or tax professional.

An example: Your IRA was valued at $10,000 and is now valued at $8,000 due to market loss. To convert your IRA to a Roth, you would pay income tax on $8,000 rather than the previous amount of $10,000. Any growth from the time of the conversion is now tax-free for qualified withdrawals.

Stay Educated

Read a book - My favorite personal finance book is the Psychology of Money by Morgan Housel. Housel provides timeless lessons about personal finance, human behavior, and long-term investing. Give it a read and let us know what you think.

Don’t:

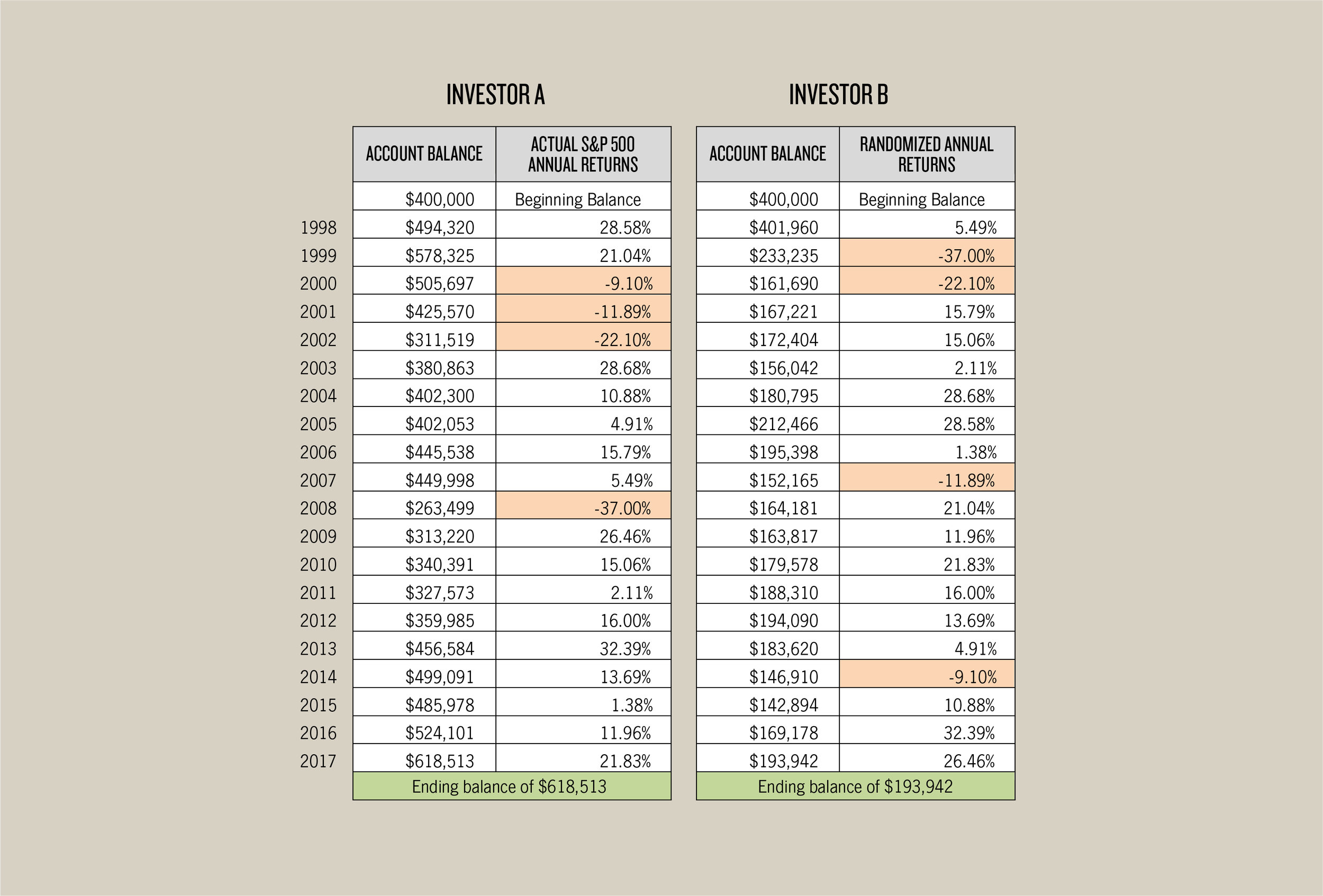

Don't invest short-term cash: Strategic cash cushions do have a significant place in a financial plan. Now is a prudent time to assess your cash holdings. Never use short-term dollars to invest.

Don't watch your account or market too closely. Staring at a screen during periods of market fluctuations can be poisonous to your emotional wellbeing. Log out, take a deep breath, and go for a walk.

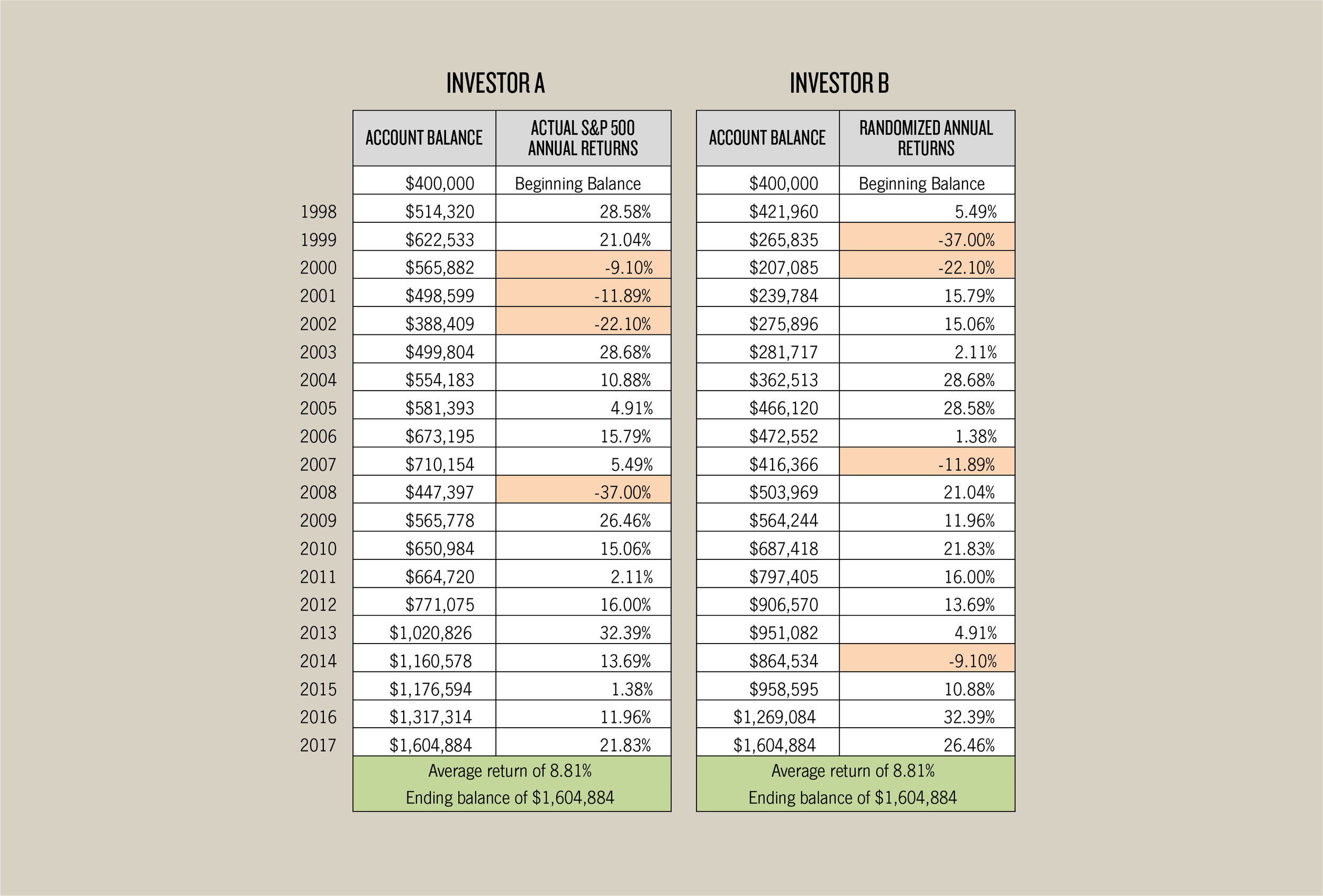

Don’t panic sell - The key thing for many investors is not to panic, stick to your plan. Remember that market declines are normal. This is the price of admission for long-term returns.

What We’re Doing for our Clients

Our team at Human Investing continues to carry our methodical approach to help steward our clients’ dollars. Our investment analyst team is constantly looking for opportunities to tax-loss harvest and rebalance. All the while, our Investment Committee persists in our due diligence for opportunities to enhance our investment strategies.

While it is important to stay the course, that does not mean you need to sit on your hands and do nothing. We hope to provide you with a list of constructive things you can do to better your financial plan. Please let our team of credentialed advisors know if there is anything we can do to help you navigate the current market.