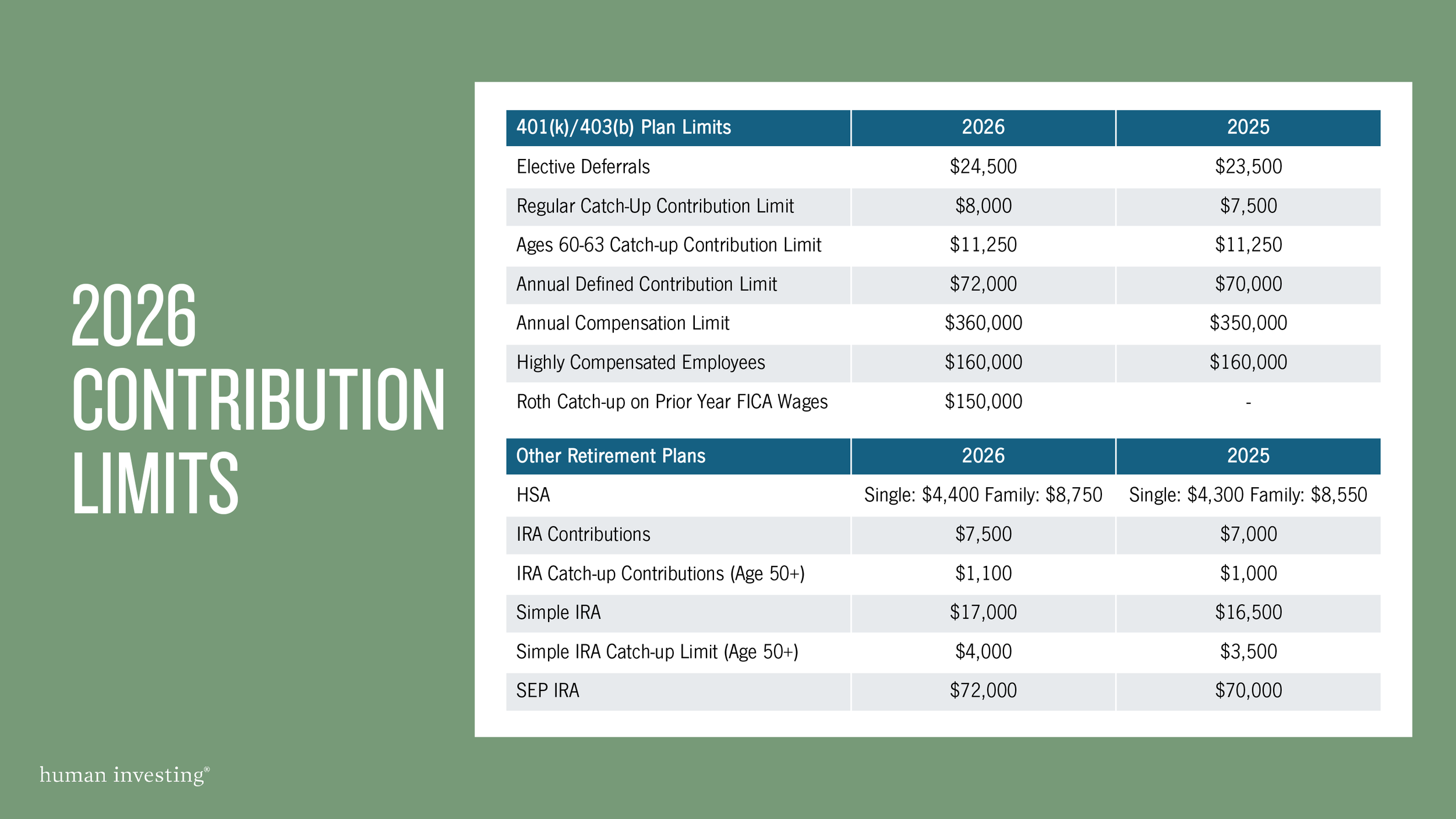

4 Reasons for Delaying Social Security

Over 50% of us take Social Security before “Full Retirement Age”… and over 90% take Social Security by “Full Retirement Age”.

What age are we taking Social Security?

Munnell, A and Chen, A, “Trends in Social Security Claiming”, May 2015, Center for Retirement Research at Boston College, from http://crr.bc.edu/briefs/trends-in-social-security-claiming/

What is “Full Retirement Age” and are 90% of people right?

Full Retirement Age or FRA is the age an individual can take their full Social Security retirement benefit without a deduction. Depending on your age this is between 65 and 67.

While the FRA to take Social Security is between 65 and 67, we can take Social Security as early as 62 with a reduction in benefits. 48% of women and 42% of men take their benefit at age 62. Is this a good idea? If your FRA is 67, by taking your benefit at 62 there is about a 30% reduction in your benefit for your lifetime. If you were normally to receive $2,000 a month, by taking it at 62 you would receive about $1,400 a month for life not including cost of living increases. Over time, this is significant.

Consider these 4 reasons for delaying Social Security:

Higher Income

If you wait until 70, your monthly benefit is significantly higher. If your FRA benefit at 66 is $2,000, then waiting until 70 will provide a benefit of $2,640. You will receive an additional $640 each month for the rest of your life plus the cost of living increases. If the $2,000 covers basic expenses, the additional $640 per month of discretionary income can be significant to an enjoyable retirement.

Survivor Benefit

If you are married, this applies to you. When one spouse passes away the survivor gets the higher of the two benefits and loses the lower benefit. Having the spouse with the highest Social Security benefit wait until 70 can drastically improve the life of the surviving partner. If you both take Social Security at FRA with one at $2,000 and the other at $1,200, when one passes the remaining spouse will lose $1,200 a month and be left with only the $2,000 benefit. Waiting until 70 for the spouse with the higher benefit of $2,640 may significantly improve the life of the remaining spouse.

Less Taxes

Social Security is not subject to tax the same way as your earned income. How much tax is paid on Social Security dollars depends on total combined income and differs from an individual to a married couple filing jointly. Whichever your situation may be, Social Security benefits are taxed either up to 50% or up to 85%. In any case, it is never taxed at 100% of the benefit. And waiting to receive your benefits until 70 may benefit the overall tax you pay. Always check with a CPA to confirm your specific numbers.

More Money

Most people will receive more Social Security dollars by waiting until 70 (If they live beyond 83.) Or if married and one of you live beyond 83, you will likely have more total dollars by waiting until 70. Additionally, if you live a long life, you will receive significantly more total dollars in retirement. This is due to the significantly higher Social Security benefit amount received by waiting, coupled with potentially lower income taxes.

Personally-saved retirement income is the base for many people’s retirement budget. If portfolio assets run out or are greatly reduced, a higher Social Security benefit can drastically impact later years of retirement to fill the gap.

Higher income, survivor benefit, lower taxes, and more money… 4 good reasons to consider waiting past full retirement age to take your Social Security benefit.

Each person, each couple is unique

There is no one size fits all in retirement planning and the ramifications of the decisions made here are significant. The questions you ask as you invest and then begin to plan towards retirement may be some of the most important, such as: what are you investing in and what are you taking your Social Security for? It's worth your time and finding trusted partners to help you navigate. At Human Investing these are the very questions we help people work through everyday for their "today's" and their "tomorrow's."