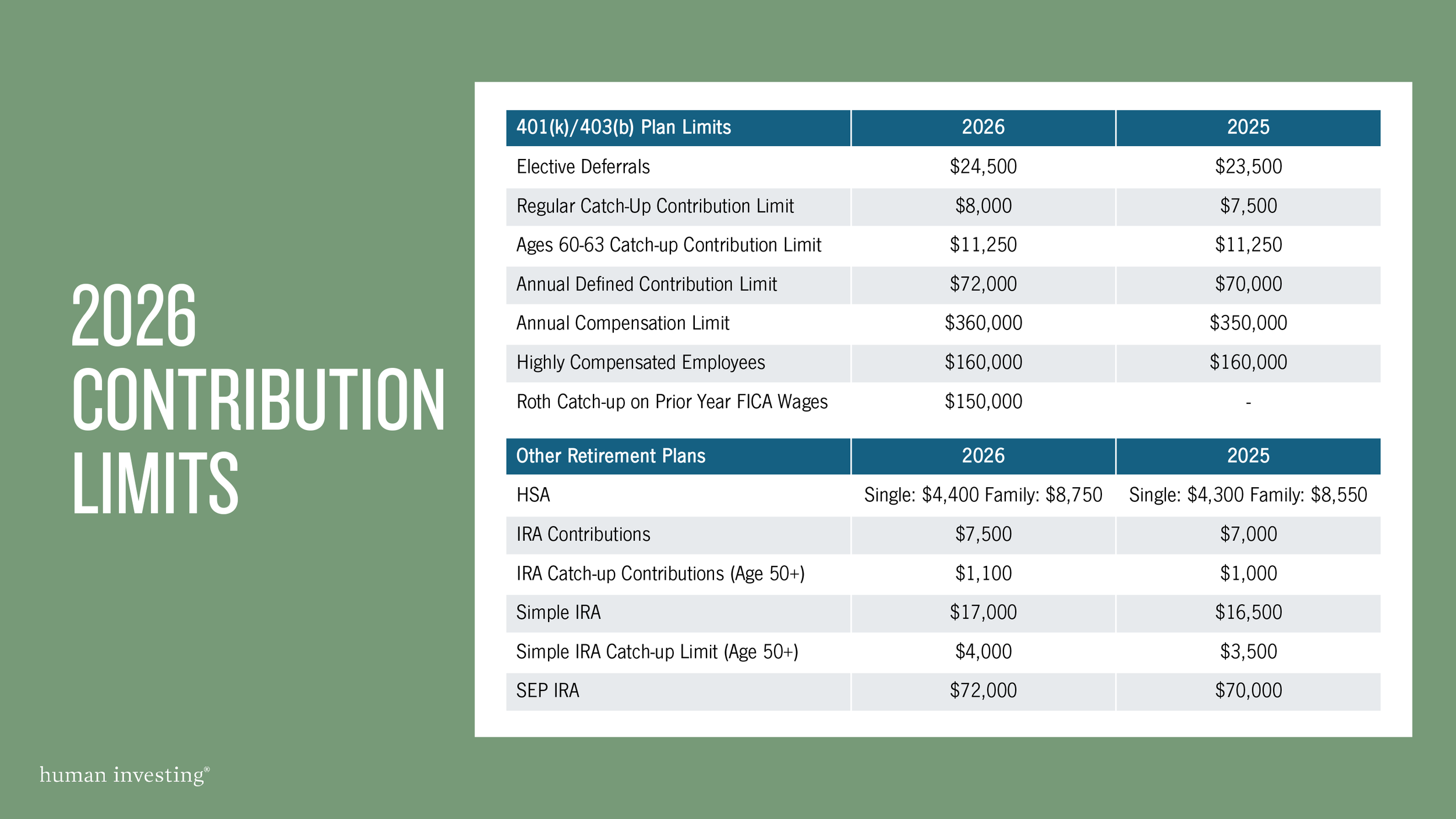

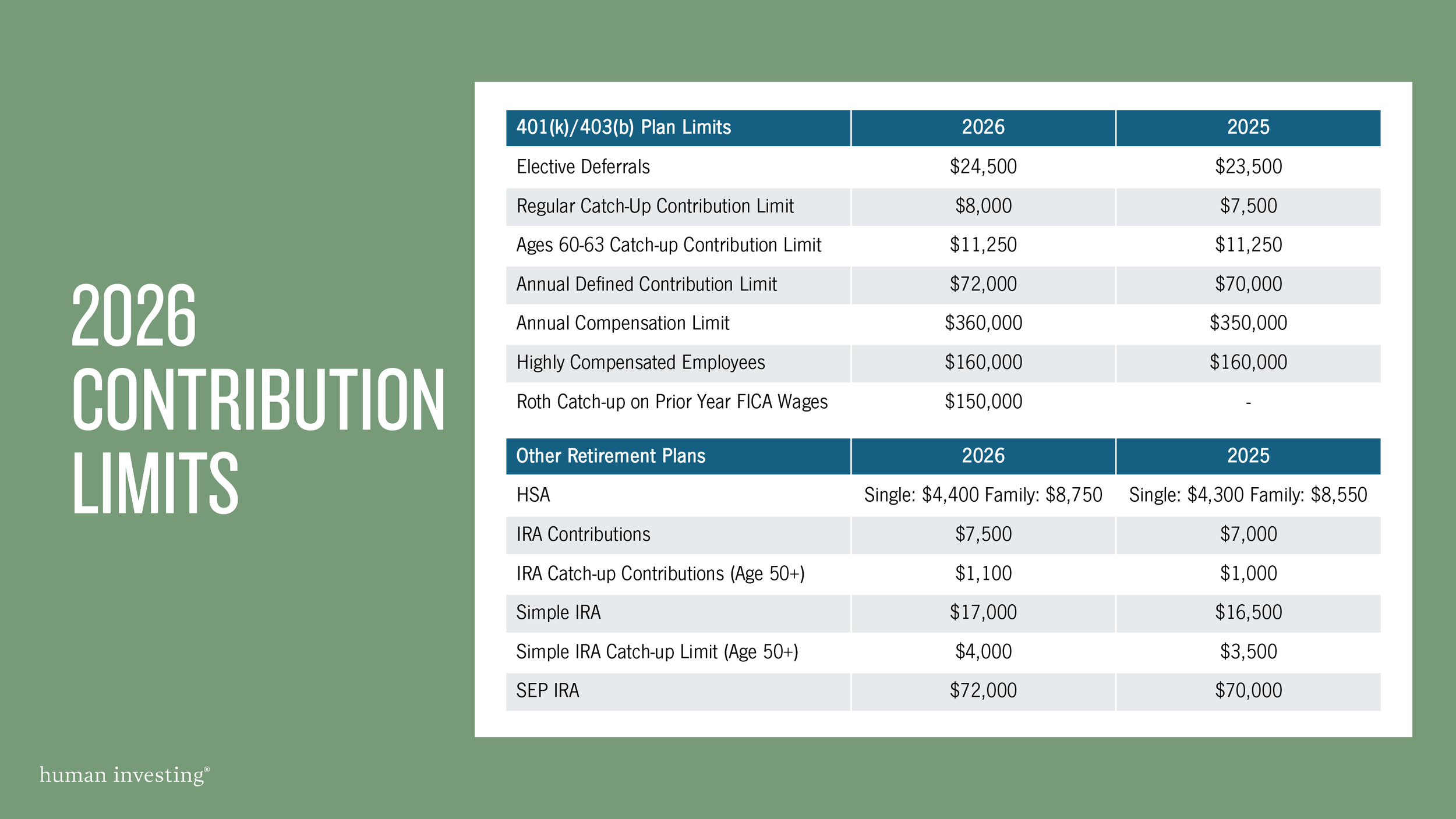

There is more good news for retirement accounts this year. The IRS has released the updated contribution limits for 2026, and several of the adjustments will allow investors to save even more. As you can see below, these new limits continue the trend of expanding opportunities for retirement savers.

Last year, we highlighted the new SECURE 2.0 rule introducing a higher catch-up contribution for employees aged 60, 61, 62 and 63. For 2026, that enhanced “super” catch-up window remains in place, giving late-career savers another year to take advantage of the increased limit.

How do these changes impact your savings in the upcoming year? Are there any changes you should be making? Schedule a time to meet one-on-one with our team. We look forward to working with you in 2026!

Related Articles

There is good news for retirement accounts! The IRS has increased the contribution limits for the upcoming year. As you can see below, there are many notable changes that will allow investors to save more money.

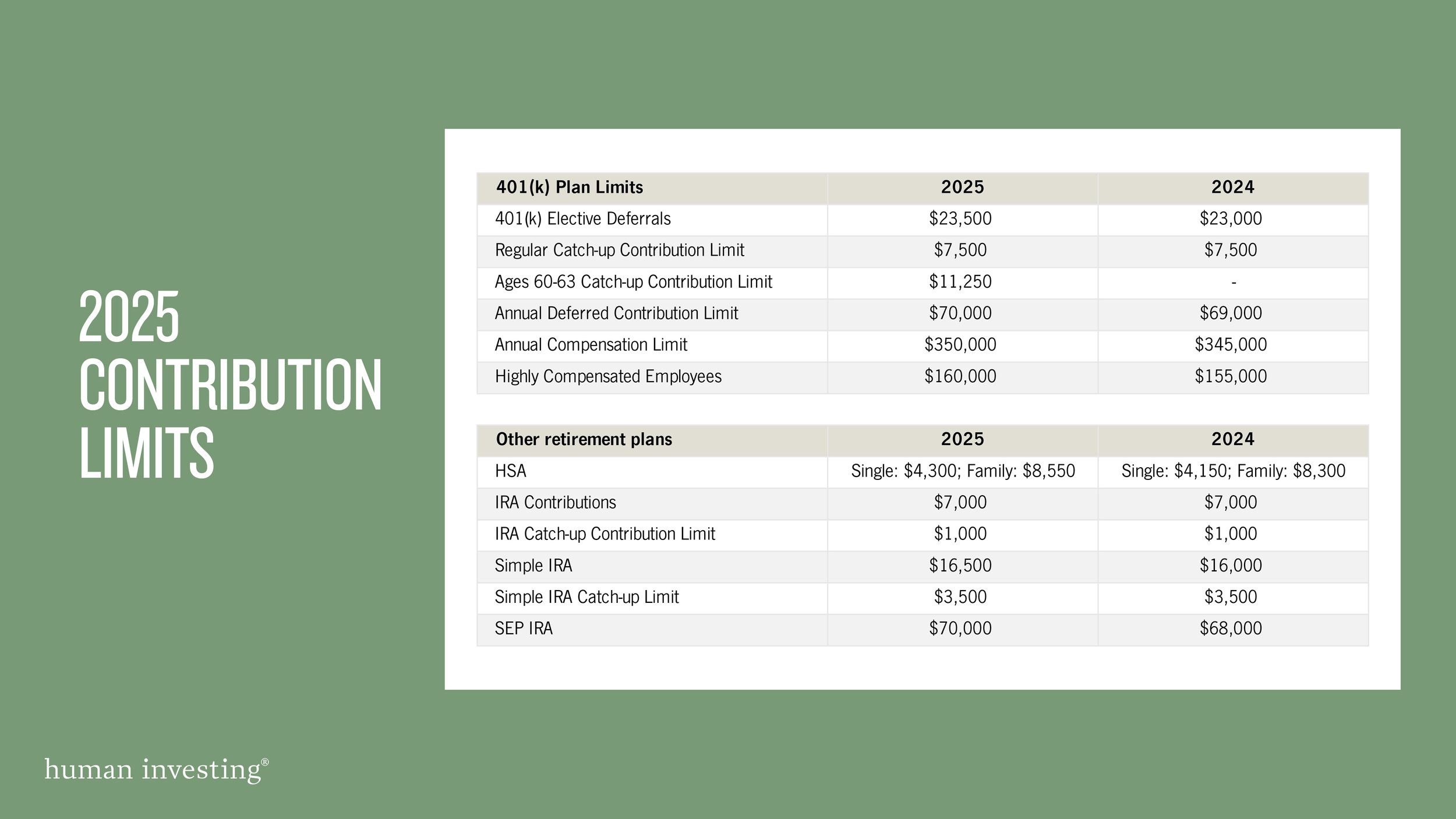

There is good news for retirement accounts! The IRS has increased the contribution limits for the upcoming year. As you can see below, there are many notable changes that will allow investors to save more money.

There is good news for retirement accounts! The IRS has increased the contribution limits for the upcoming year. As you can see below, there are many notable changes that will allow investors to save more money.

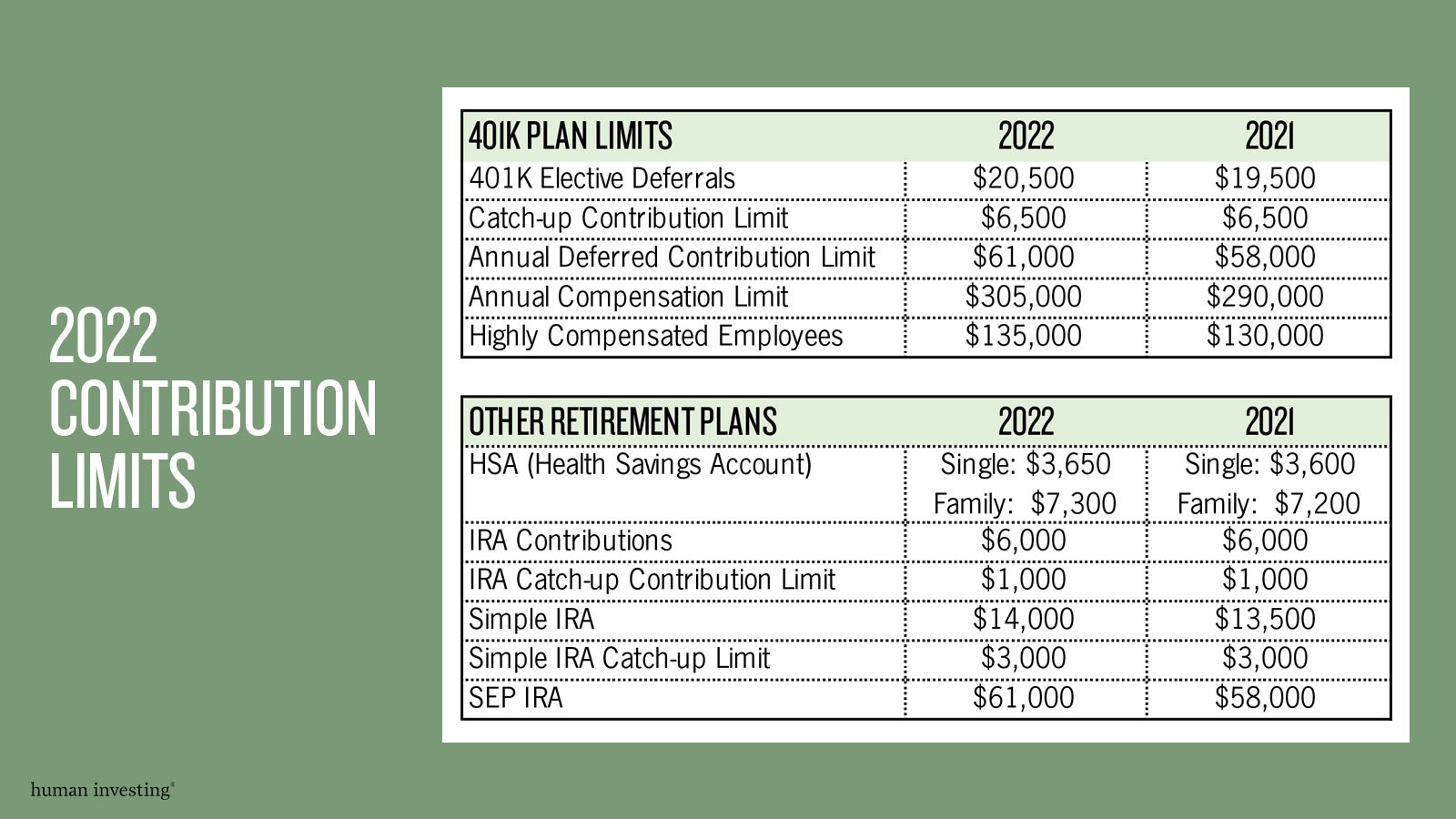

There is good news for retirement accounts! The IRS has increased the contribution limits for the upcoming year. As you can see below, an important change for 2022 is that 401(k) elective deferrals increased from $19,500 to $20,500. That’s not all! Read more for the applicable updates for the coming year:

Transitioning into retirement can be an exciting time. For many it can also be a daunting reality. We hope the following Pre-Retirement Checklist is a helpful as you intentionally prepare for your retirement years.

Saving for retirement can seem straightforward compared to the daunting task of converting your hard-earned savings into retirement income. When building a retirement income plan knowing what questions to ask will potentially save you money, lower your overall tax bill, and provide you peace of mind.