Recently, our office had a fun, lively debate, centered around the question: “What is the opposite of fire?” Answers varied from ice, water, not fire, etc. This question inevitably raised another question – What does it mean to be an “opposite?”

Personal finance has a version of this problem: paying down debt versus saving for the future are routinely framed as opposites.

Each of us has our own beliefs around money. Some of this has been shaped by our family of origin, how we were raised, or by our lived experiences as adults. My family of origin always emphasized debt as something to be eliminated at all costs and as aggressively as possible. Personal finance experts like the one-and-only Dave Ramsey would agree.

Wanting debt paid off as soon as possible is a very human instinct. A client recently told me “We’ve been putting extra money towards paying off our mortgage. It just feels good to see the balance go down.” Debt can feel heavy and limiting. As another client once succinctly shared, “Loans make me sad.” And with Americans now carrying more household debt than at any point in history, that weight is only growing.

But in personal finance, sometimes doing what feels responsible can actually cost you.

Debt Paydown Is a Form of Saving

Recent Vanguard research asserts that “paying down debt is a form of savings, just like saving for an emergency fund or retirement.” They aren’t opposite. In recognizing this, we can now reframe our decision making and give each of our dollars a specific job.

Rather than thinking in separate and distinct categories such as paying off debt, saving for emergencies, or saving for retirement, you can simply ask “Where is my next dollar most effective?” Some of our previous blogs have broadly explored this idea, but I’d like to get specific.

Two Debt Mistakes That Hurt Long-Term Wealth

My Grandpa Leo would say, “All debt is bad,” and maybe you feel similarly. However you feel about debt, the fact is not all debt is created equal, and debt differs in amounts, interest rates, terms, etc. Your payoff strategy and financial plan should reflect these details and nuances.

Although debt differs, Vanguard outlines two patterns that show up consistently regarding debt that generate a negative impact in someone’s lifetime net worth:

Paying Down High-Interest Debt Too Slowly

Paying Down Low-Interest Debt Too Quickly

The patterns are counterintuitive: most people are simultaneously moving too slow on the debt that hurts them the most long-term, and too fast on debt that isn't. Getting the sequence right can meaningfully change your financial outcome over time.

Before we go further, a quick frame of reference. When we refer to 'high-interest debt,' we mean anything with an interest rate at 7% or higher. That number comes from the historical long-term return of a diversified investment portfolio. If your debt costs more than your investments are likely to earn, paying it down first wins. We'll use this as a benchmark throughout. Actual returns over time may vary.

Let’s explore each debt paydown mistake together.

Mistake #1: Paying Down High-Interest Debt Too Slowly

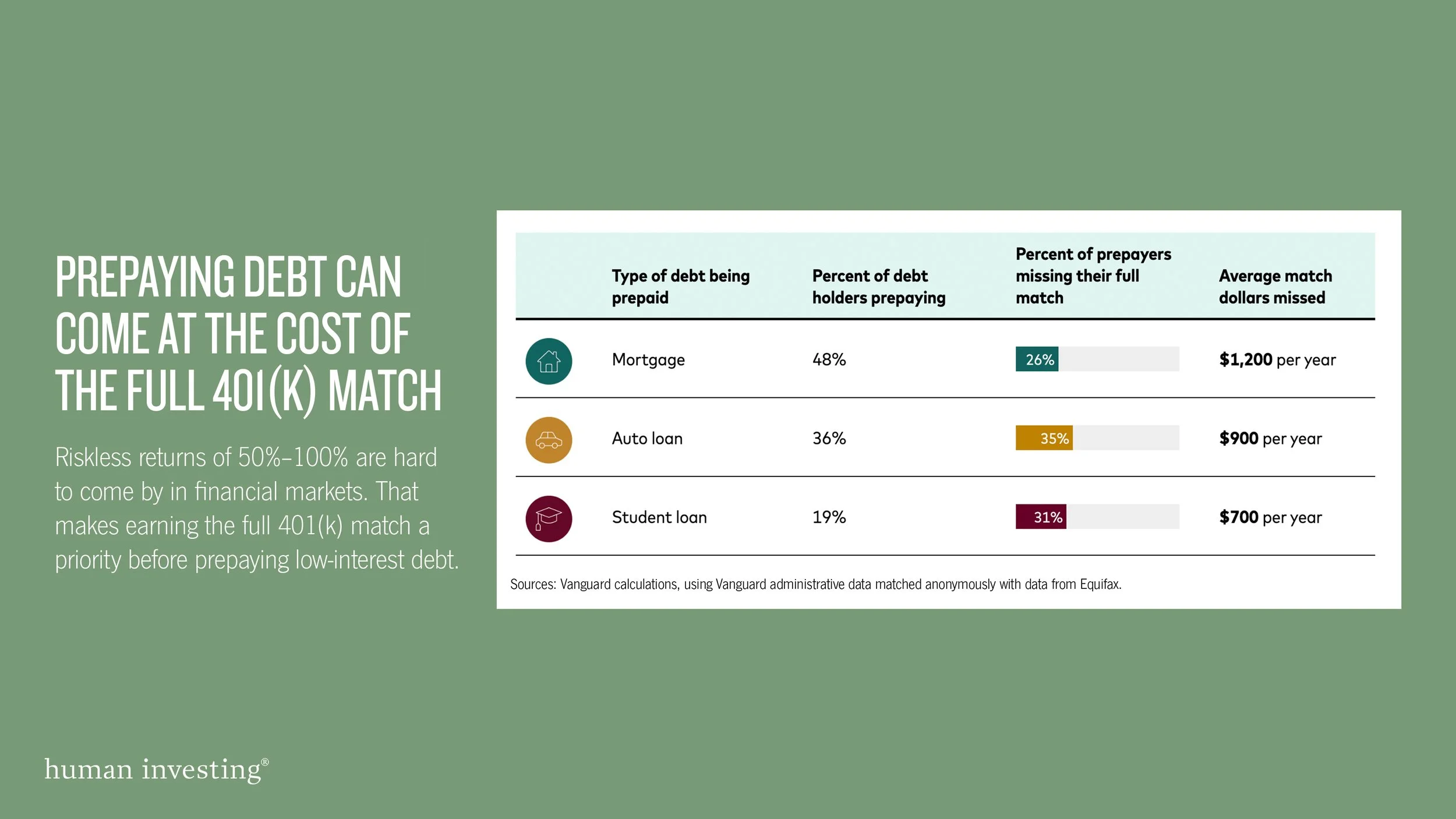

About 35% of investors carry revolving credit card debt — balances that roll month to month and compound at high interest rates. What Vanguard found is that many of these same households have money sitting in savings earning underwhelming returns, are making additional unnecessary payments on lower-interest loans, and are over-contributing to their 401(k) beyond the employer match.

In other words, they have the resources to wipe out their most expensive debt. They're just directing those dollars somewhere else.

This is rarely intentional, and it's more common than you'd think (see chart below). It's what happens when financial decisions get made in isolation. Each one feels reasonable on its own (paying down a loan, building up savings, maxing out your retirement), but without a coordinated strategy, those dollars aren't working together. They're working against each other.

Mistake #2: Paying Down Low Interest Debt Too Quickly

Many people make aggressive payments on mortgages, student loans, and auto loans — debts with interest rates below 7%. While your intention may be good, the math doesn’t always support it.

What Vanguard found is that many of these same households are leaving employer 401(k) matching contributions on the table, investing less than they could, and drawing down cash reserves.

The cost of that tradeoff is real. For a worker earning a median income of $81,000, prepaying a low-interest debt for 10 years while missing out on the full employer match could mean an estimated $120,000 less at retirement. That's not a rounding error.

As the chart below shows, decisions that feel productive in one area can quietly limit your progress in another.

Why Emotion Drives Most Debt Decisions

Financial decisions are not just about math. Behavioral and emotional components have a strong influence in our decision making. I would argue this isn’t necessarily a bad thing. It’s a human thing.

The emotional pull of debt shows up in conversations constantly. Clients say things like:

“I just want to get rid of all my debt as quickly as possible.”

“I can’t invest until I am totally debt-free.”

“My student loans bother me more because the balance is bigger. I want to tackle those instead of the tiny balance on my credit card.”

These feelings are valid but they can lead to decisions that don't reflect the full picture, like ignoring a high-interest credit card because the balance feels manageable.

Your history with money shapes how you make these decisions. Being honest about that is actually the first step toward a better strategy. Instead of applying a single rule, the goal is sequencing. Knowing which dollar goes where, and in what order, makes the whole system work.

How to Sequence Your Debt Paydown

Here are the starting points, drawn from Vanguard's research:

1. Prioritize your 401(k) employer match before paying down debt.

This is my favorite financial move with a guaranteed return, typically 50–100% on your contributions. If you're not capturing the full match, you're leaving money on the table. This takes priority even before paying down high-interest debt, because no debt payoff strategy outperforms free money.

Pay off debt or save for the future?

Invest it or pay off the loan?

$10,000 over 30 years — investing at 7% vs. a 4% loan balance

Starting value: $10,000. Investment returns are hypothetical and not guaranteed. Past performance does not predict future results.

2. Pay off high-interest debt (7% or higher) aggressively.

Credit card balances and similar debts compound quickly and quietly. Once eliminated, those payments free up real cash for investing, saving, or whatever comes next.

If this step feels out of reach, you're not alone. Nonprofits like GreenPath Financial Wellness can help you pay down consumer debt, lower your interest rates, and access free financial counseling.

Pay off debt or save for the future?

The price of ignoring high-interest debt

$10,000 over 30 years — three scenarios compared

Starting value: $10,000. Investment returns are hypothetical and not guaranteed. Past performance does not predict future results. Loan/debt figures assume no payments made.

3. Weigh investing against paying down low-interest debt.

Once you've captured your match and cleared high-interest debt, the next question is whether extra dollars are better used paying down a low-interest loan or going toward long-term investing. Money invested in your 401(k) or Roth IRA is likely to outperform the cost of that debt over time. It might not feel as satisfying in the short term but the math tends to win.

A Better Way to Think About Debt

These steps don't exist in isolation. A debt paydown strategy is one piece of a personalized financial plan. When your debt, savings, and investing decisions are coordinated, your dollars work harder and your progress compounds over time. And not to mention, it feels much better.

Want to chat through your prioritization of a dollar, or how to approach your debt paydown strategy? Let’s connect!

Disclosure: Human Investing is an SEC-registered investment adviser. Registration does not imply a certain level of skill or training. This content is for informational and educational purposes only and does not constitute personalized investment advice or a recommendation. Past performance is not indicative of future results. All investments carry risk, including potential loss of principal. Readers should consult with a qualified professional regarding their specific financial situation.