You went into medicine to care for people. But somewhere between the 80-hour weeks, the charting backlog, and the six-figure loan balance that keeps growing while you sleep, the work of being a doctor can start to feel like it's costing you the very life you wanted to build.

We can't fix the system overnight, but we can take one major source of stress and bring it under your control: your finances. For early-career physicians, getting clear on your money is one of the most powerful things you can do for your long-term wellbeing. Clarity creates the bandwidth to keep doing the work you trained so long to do.

The Decade to Get Right

The first ten years are a blur: residency, maybe fellowship, then your first attending role. They're also the years that quietly shape the next thirty.

The financial question that dominates this stage is student debt. The average medical school graduate now carries close to $225,000 in loans. Meanwhile, the average first-year resident earns $68,166, climbing only to $73,301 by PGY-3. The math doesn't work for traditional repayment, which is why most residents either defer or enroll in an income-driven repayment (IDR) plan.

Both are reasonable approaches that require thoughtful planning. Dr. Tricia James, Director of the Clinician Experience Program at Providence, notes that multiple studies link rising student debt directly to physician burnout, which means this isn't just a math problem, it's a wellness problem.

Here's why starting early matters more than most residents realize: every month you spend in an IDR plan during training is a month of the lowest payments you'll ever make. If you pursue PSLF, those payments count toward your 120. Even if you don't, you'll have kept interest from snowballing and put yourself in a stronger position whichever path you choose.

Considering Public Service Loan Forgiveness

Every physician with federal loans should at least consider PSLF. Whether it's the right move depends on your career path, your specialty, and where you choose to practice. The clearest way to see how it plays out is to look at two physicians on opposite ends of the spectrum.

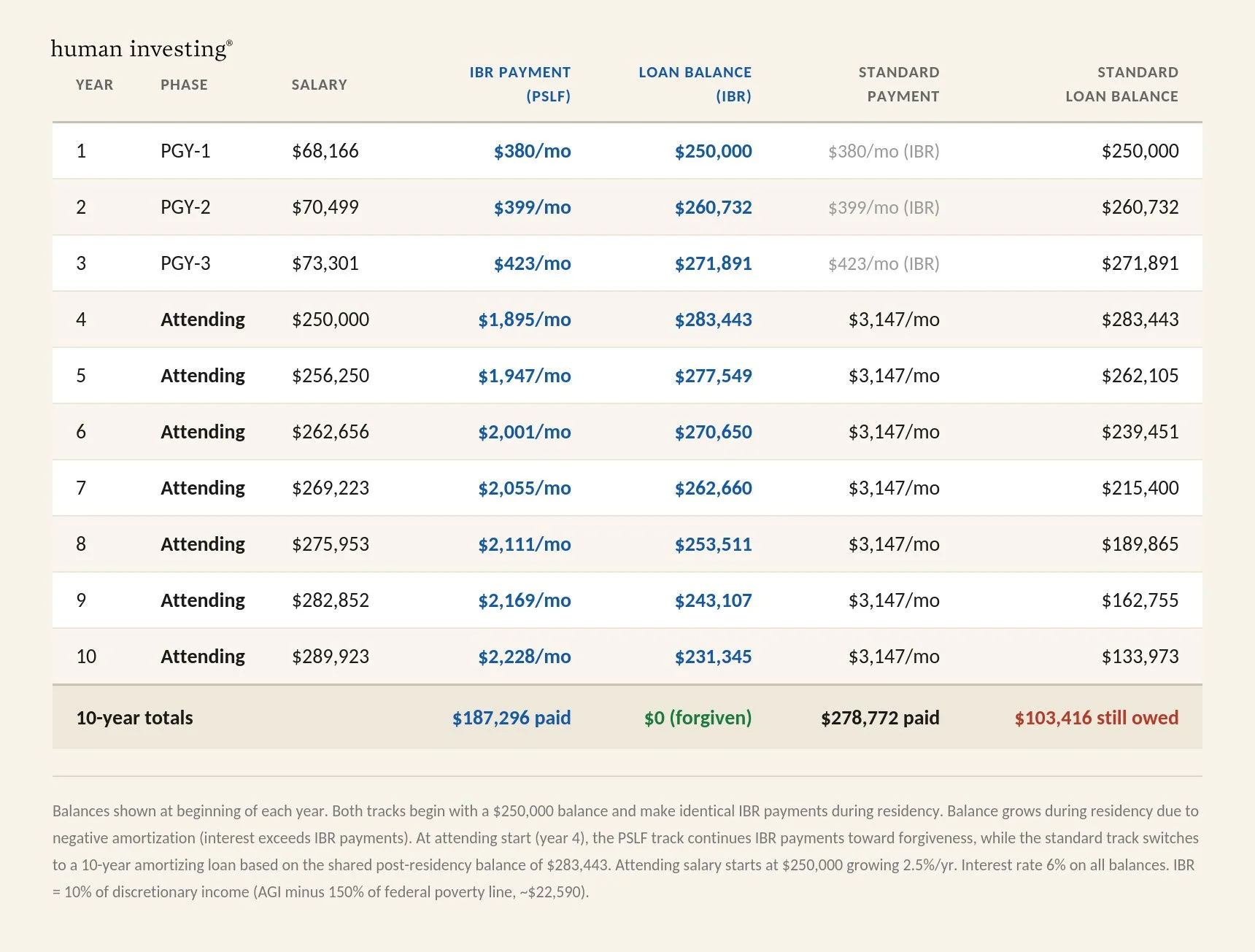

When PSLF clearly works: Imagine Sarah, a family medicine resident finishing training at an academic medical center with $250,000 in student debt. Throughout her three years of residency, she makes IDR payments capped at 10% of her discretionary income, modest payments that barely dent the balance. By graduation, interest has pushed her total debt to $283,443.

Here's where PSLF starts doing its real work. Sarah stays on as an attending at the same nonprofit system, earning $250,000. Her payment adjusts upward with her income, and she continues making qualifying payments for another seven years. At the end of that decade, the remaining balance (still substantial) is forgiven. Sarah never pays off the principal, and she doesn't need to.

PSLF was built for exactly this kind of career:

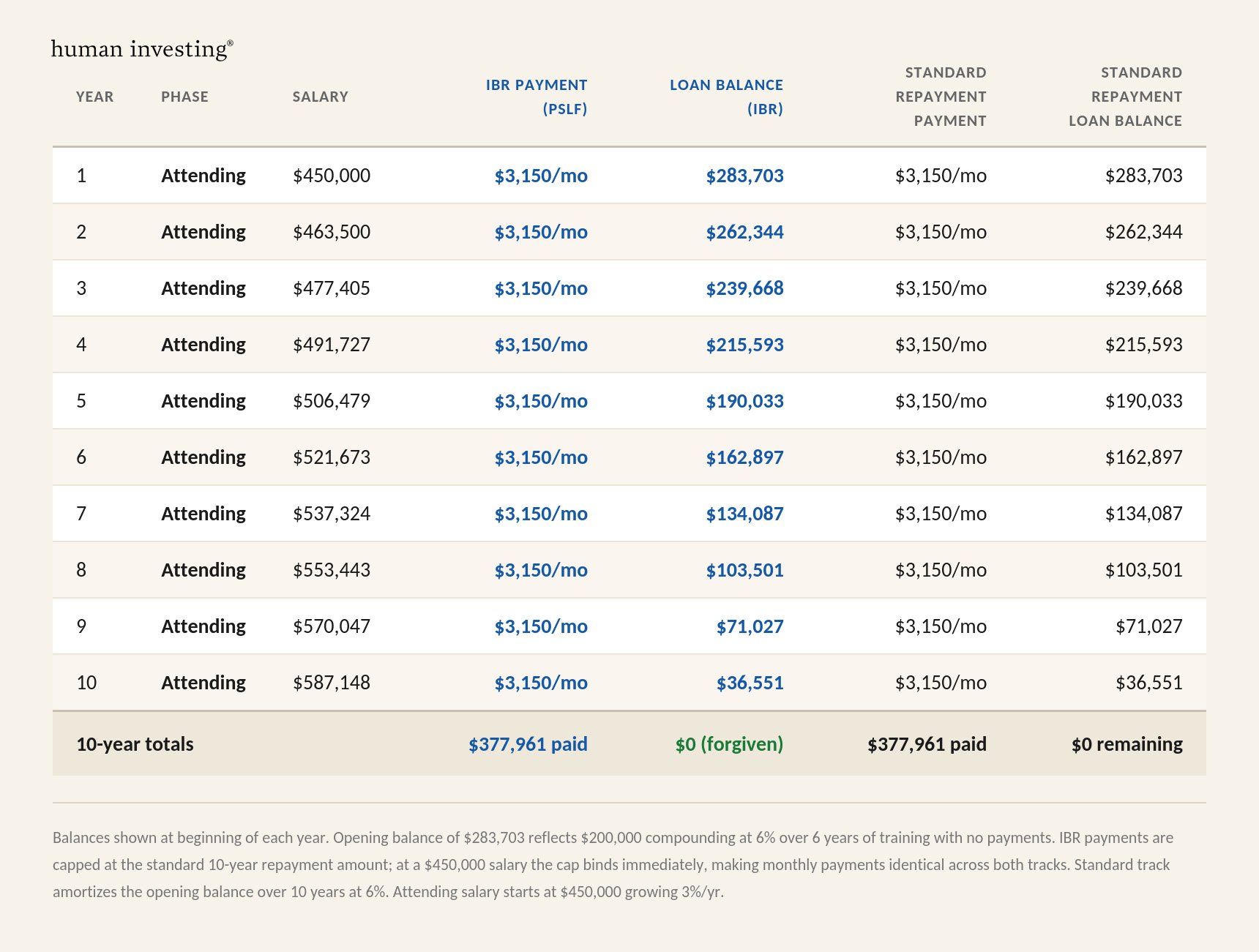

When PSLF works against you: Now imagine David, a cardiology fellow finishing training with $200,000 in debt. Unlike Sarah, he defers his loans during fellowship, and by the time he's hired, a 6% interest rate has grown his balance to $283,703. He takes an attending role in private practice at $450,000.

At that income, IBR caps his payments at the standard 10-year repayment amount, meaning PSLF offers him no real benefit. He'd be better off refinancing to a lower rate, paying aggressively, or doing both. Skipping PSLF also keeps the door open to private-practice opportunities, where long-term compensation often exceeds what nonprofit work pays.

The takeaway: PSLF is a powerful tool when your specialty, employer, and income align. Part-time work, the program's 30-hour-per-week minimum, employment gaps for family, and switching practice settings all change the calculus, which is why this decision deserves real attention early in your career, not after the fact.

Concerns About the Future of PSLF

PSLF has been politically contested for years, and it's fair to wonder whether the program will still be intact by the time you've made your 120 payments.

A few things worth knowing: PSLF is written into the promissory notes you sign on federal loans, which makes wholesale elimination legally messy. If lawmakers do change the program, history suggests changes are more likely to apply prospectively than retroactively. And any meaningful legislation takes years to pass and implement. As of this writing, no serious proposal would block physicians from participating.

One more thing worth reinforcing: even if you ultimately decide PSLF isn't your path, the residency-era strategy is the same. Making qualifying IDR payments during training protects you against interest accumulation and preserves your options. It's the rare financial move that works in your favor under almost any future scenario.

Starting Down the Right Path

If you're entering residency, these are the steps we recommend at Human Investing, starting on Day 1:

Confirm you qualify. Eligible employers include federal, state, local, and tribal governments; public education; public health; and 501(c)(3) nonprofits. Only federal direct loans count; other federal loans need to be consolidated.

Enroll in an IDR plan and start paying immediately. This is the single highest-impact move you can make in training. Every resident with federal loans qualifies for an IDR plan, and on a resident's salary, your monthly payment may be surprisingly low, sometimes only a few hundred dollars. The size of the payment doesn't matter; every qualifying month counts the same toward your PSLF 120. There's no good reason to wait.

Capture the match. Contribute enough to your employer's retirement plan to get the full match. Pre-tax contributions also lower your AGI, which lowers your monthly loan payment. That's a rare win-win.

Invest beyond the match as your budget allows. Time is the single biggest advantage you have right now.

Taking Care of Your Future Self

The physicians who sustain long, meaningful careers tend to be the ones who built clarity into their financial lives early, so that money became a tool rather than a burden. That's the goal: not wealth for its own sake, but the freedom to keep showing up for your patients, your family, and yourself.

To learn more about the Clinician Experience Program at Providence, including coaching, peer groups, and leadership development designed specifically for clinicians, visit the Providence Clinician Experience Program.

This is the first in a co-authored series on financial wellness as a core component of clinician wellbeing, covering each major stage of a physician's career.

Disclosure: Human Investing is an SEC-registered investment adviser. Registration does not imply a certain level of skill or training. This content is for informational and educational purposes only and does not constitute personalized investment advice or a recommendation. Past performance is not indicative of future results. All investments carry risk, including potential loss of principal. Readers should consult with a qualified professional regarding their specific financial situation.