Earnings season is coming

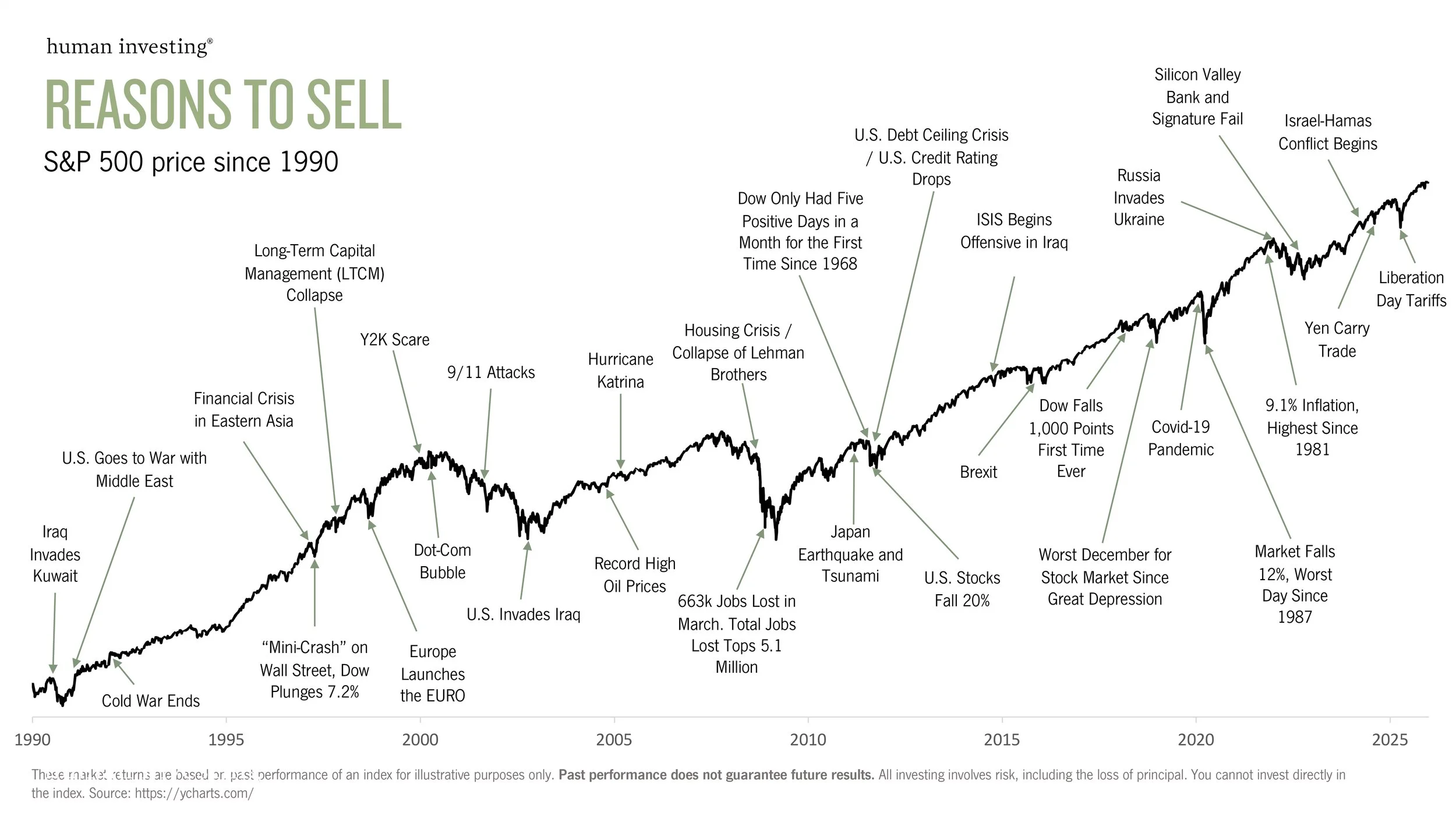

Nike’s stock price has been struggling, for several years now. You have to go back to the early 2000s to find a time when it took Nike longer to hit a new all time high. With that, many Nike employees are wondering what to do with their stock. Whether it is to diversify into another investment or to fund expenses like vacation, remodels, or tuition for their kids, the current price has made those decisions more difficult. A common question we hear is “Should I sell my NKE now or wait?”

NKE has recently experienced declines. From Jan 2025 to Apr 2026, NKE fell -41.60% while the S&P 500 has risen 22.57%. Nike had a great run of outperforming the S&P 500 for 10 out of 12 years prior to 2021 but has been on a losing streak since.

Is Nike poised to make a comeback? Predicting the future of any stock, or the market overall, is a difficult task. Nike is the industry leader in athletic apparel, particularly in footwear. If Nike can maintain their brand and industry leadership, they are poised to be successful. Achieving outperformance relative to the S&P 500 is not guaranteed.

Let’s look at a few different ways to approach valuing a stock to get a sense of if NKE appears over or undervalued.

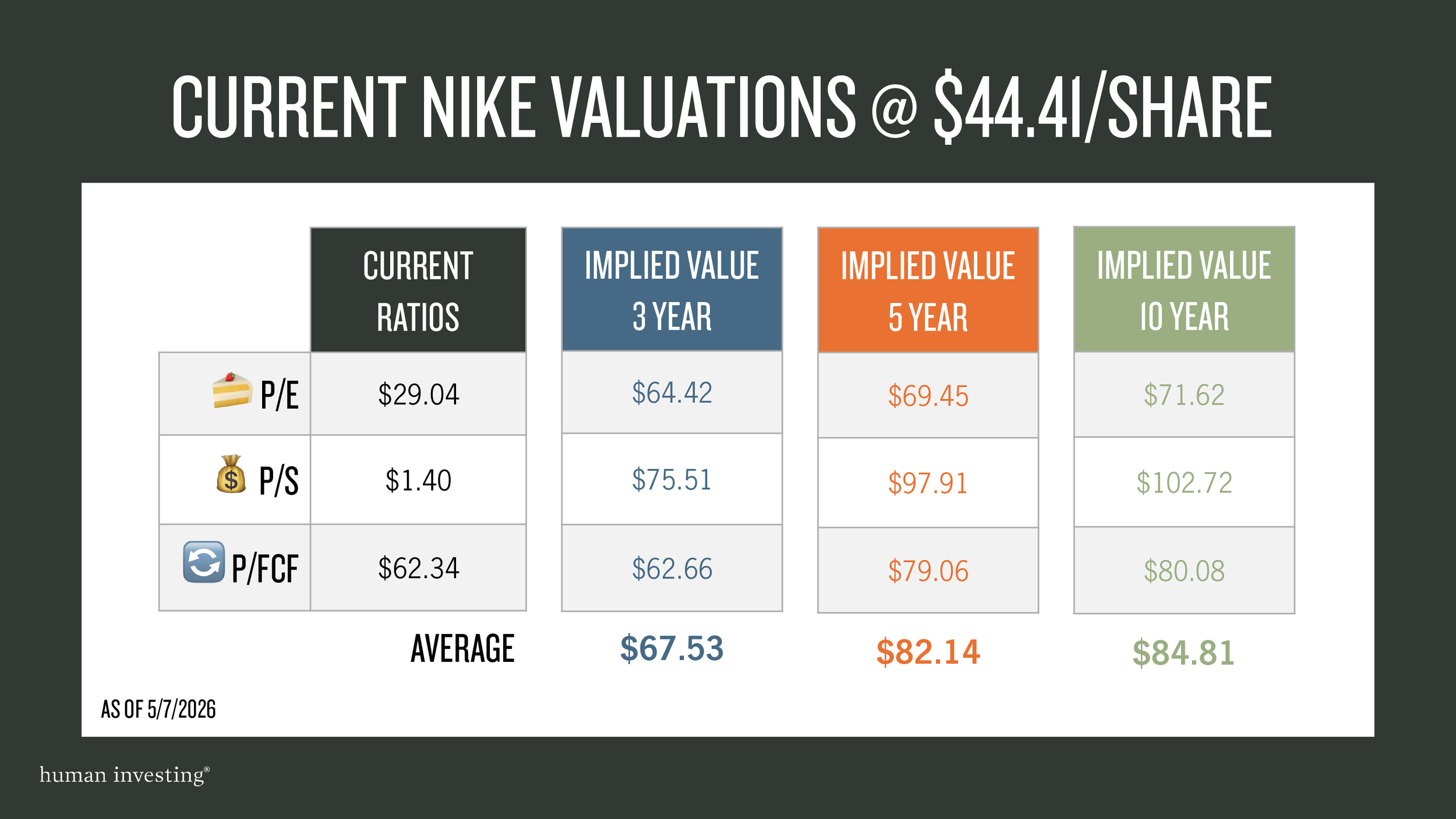

🍰 Price / Earnings (P/E) ratio - how much are you paying for each dollar of earnings:

Pros: Earnings are the profits of the company, and those profits are ultimately what is available for shareholders as dividends

Cons: Easily manipulated or adjusted by many line items on the income statement, can vary greatly year to year

Current P/E: 29.04

3 year median P/E: 29.78

Implied Valuation based on $2.16 Earnings Per Share = $64.42

Verdict: Based on this metric, NKE appears below its historical median valuation.

💰 Price / Sales (P/S) ratio – how much are you paying for each dollar of revenue:

Pros: Less subject to manipulation or fluctuation

Cons: Doesn’t consider efficiency (i.e. costs necessary to generate the revenues)

Current P/S: 1.40

3 year median P/S: 2.40

Implied Value based on $31.45 revenue per share = $75.51

Verdict: Based on this metric, NKE appears below its historical median valuation.

🔄 Price / Free Cash Flow (P/FCF) ratio - How much are you paying for each dollar of operating cash:

Pros: Shows cash actually available to investors for dividends or stock buybacks, ignores non-cash expenses (i.e. depreciation)

Cons: Still subject to manipulation based on accounting practices, can vary greatly year to year

Currentl P/FCF: 62.34

3 year median P/FCF: 28.52

Implied value based on $2.20 free cash flow per share = $62.66

Verdict: Based on this metric, NKE appears below its historical median valuation.

🥣 Average of all ratios:

Take the average of the implied values for P/E, P/S, and P/FCF

Implied Value = $67.53

Verdict: Based on this metric, NKE appears below its historical median valuation.

🚀 Price / Earnings Growth (PEG) ratio = P/E ratio / Earning Growth – measure P/E in context of company’s growth rate

PEG < 1 implies undervalued, PEG > 1 implies overvalued.

Currently: 29.04 / -30.88 = -0.94

Decrease in EPS results in negative value, and less than 1 means the earnings are shrinking faster than the P/E ratio; bad all around

Forward 1 year: 2.53

Verdict: NKE is poised to be successful.

Based on historical averages, NKE currently appears undervalued

That is typical for a stock that has been declining in earnings and price over time.You can also take different time periods for the median of these valuations, to see what Nike’s valuation has been like over a longer period of time.

Note: All data courtesy of YCharts as of: 5/7/2026

While Nike may appear undervalued on a 3-year basis, the difference is greater over 5-year and 10-year medians. If you’re thinking about selling, these valuations may give you some guideline thresholds to re-evaluate at.

Based on historical averages for NKE, the stock currently appears undervalued. The decline in NKE’s price in recent years is a big reason for that. Whether the decline will continue, or NKE will return to its historical valuation norms nobody knows. Looking at the basic fundamentals, NKE has some clear struggles. 2025 fiscal year saw declines from 2024, which is unusual and not a healthy sign. On the other end, the basics of continuing on as a business seem strong for NKE:

NKE has consistently sold its products above the cost of those goods.

NKE can cover both its current and longer-term debt needs based on existing cash and future expected earnings.

NKE has not missed a dividend in the past 10 years.

These metrics are by no means the only way to approach whether now is a good time to sell your NKE stock. Other factors to consider:

The amount of time you think you will work at Nike.

How much of your Net Worth is tied to NKE?

When do your Stock Options expire (if applicable)?

Your comfort level with the ups and downs over time.

Do you have any major expenses coming up? i.e. house purchase, funding college, etc.

We’re here to help

Beyond these factors and metrics, it is important to integrate your Nike stock decisions within the context of a comprehensive financial plan. If you have questions or would like to discuss whether to hold or sell your NKE stock, please reach out to us at nike@humaninvesting.com.

Disclosure: This material is for informational and educational purposes only and should not be considered personalized tax, legal, or investment advice. You should consult your own qualified tax, legal, and financial professionals before making any decisions based on this information. Tax laws and regulations, including those related to bonuses and supplemental income, are subject to change and may vary depending on individual circumstances. The examples provided are hypothetical and intended to illustrate general tax concepts; they should not be relied upon to determine your actual tax liability. Investing and financial planning involve risk, including the possible loss of principal. Past performance does not guarantee future results. Advisory services are offered through Human Investing, LLC, an SEC-registered investment adviser.