Demand for better financial literacy is going up

Financial Literacy is the understanding of financial concepts which guides good money decisions in everyday life.

The backdrop of personal finance is having a structure for how to act. We usually refer to this as a financial plan. A financial plan helps to allocate money, a limited resource (for most of us), to unlimited alternatives.

Financial literacy can help parents make a difference

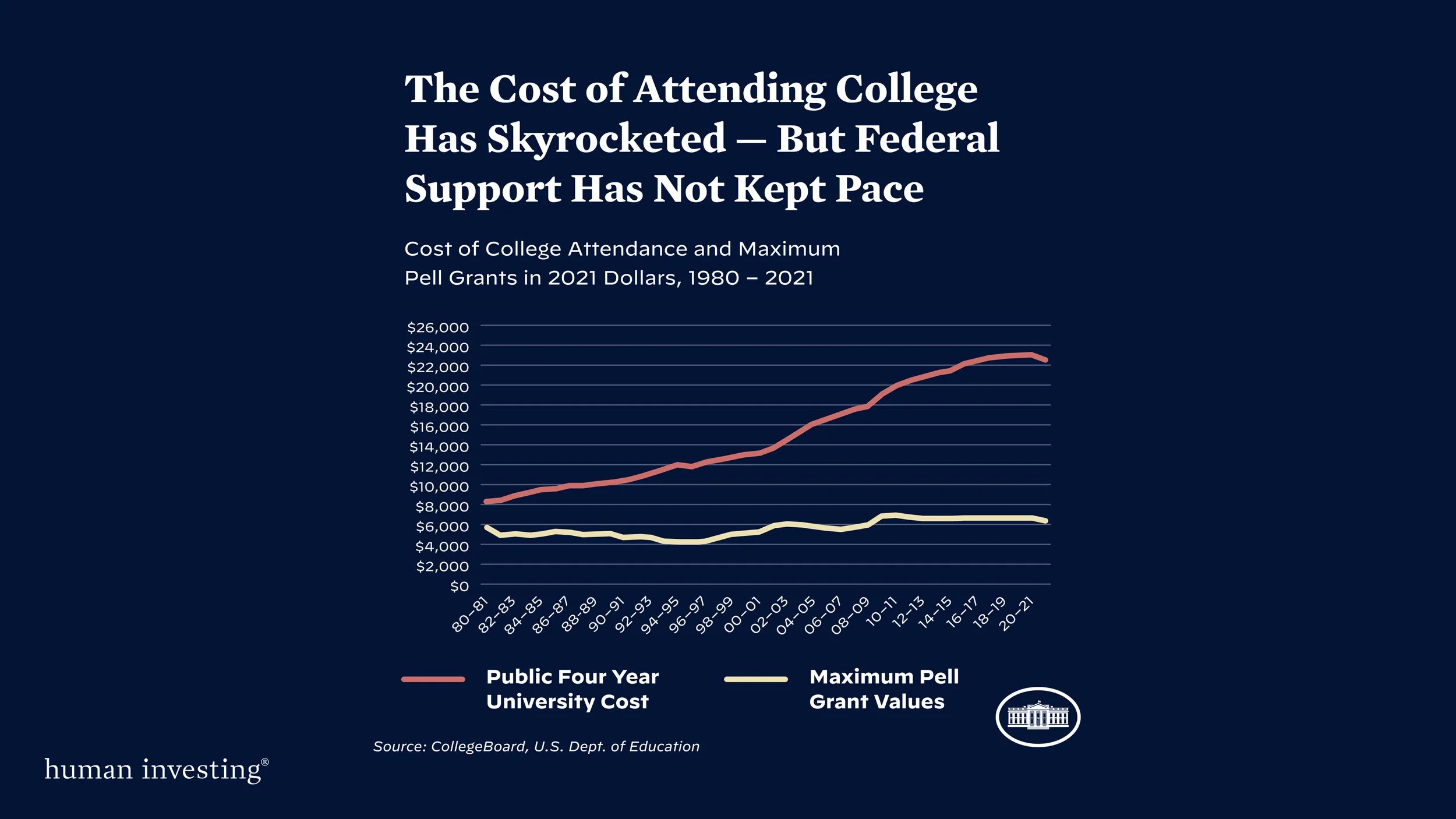

The United States is the largest economy in the world however, Standard and Poor’s Global Financial Literacy Survey reveals that it is the 14th in the world in Financial Literacy at approximately 57%.

By age 7, most children begin to grasp that money can be exchanged for goods and represent value. For example, understanding that 5 pennies equals 1 nickel, as a University of Cambridge research on “Habit Formation and Learning in Young Children” discovered. Starting at age 7 or 2nd grade, a child is ready for more instruction and guidance around money concepts. In the same way that children learn language from their parents, they can and do learn money habits from their parents but need exposure and instructive conversations. Moreover, children need the opportunity to practice with money, or forms of money, that have different representations of value.

Financial literacy can lead to responsible decision making

Parents have the ultimate authority and responsibility to begin educating on financial concepts from a young age. Parents should be aware not to rely on the education system to teach the basics or complexities of personal finance, as it is not required to graduate in many states (ex: Oregon).

To help empower parents with the knowledge and tools to provide a great foundation for personal finance, let us refresh ourselves of the basics of what children can learn and apply early in their formation. Always remember to keep it simple.

Start with an approachable framework

The four basic functions for allocating money is to Spend, Save, Invest, or Give. A guideline to start with is a 30/70 rule: save, give and invest 30% while spending the remaining 70%. To create a basic guideline for our kids (and possibly even ourselves), let’s break each of these functions down.

The heart of giving

Let’s start with giving, since many of us have experienced that if it is not given up front, it may not be given at all. This is important in establishing an altruistic worldview (selfless concern for the wellbeing of others) but also in teaching an abundance mindset (always more to go around) as opposed to a scarcity mindset (only so much and never enough). Giving can immensely impact a child’s desire to be a force for good and help others, which is the foundation for business. When banking a dollar per week from allowance, even with this small amount, it can be a great place to start the heart-healthy habit. Ask your child what they care about and who they would like to help with their giving, it may surprise you.

The necessity of saving

A similar principle will prove necessary for saving. It is much easier to set aside some money prior to spending to ensure you will have something left over when needed. Having adequate savings can keep you from being subject to predatory lending or missing out on an opportunity. It is equally important to help kids understand that saving is not the same as investing. It is important to have money working for you, not just set aside and available to you.

The value of investing

The importance of investing is compounding interest and seeing your hard-earned dollars multiply for you in a way that seems effortless but requires patience and self-control.

Setting money aside to help a child invest in a company like Disney or Nike, something they can tangibly see and enjoy, is a great learning lesson. This could be done through your taxable investment account or in their own UTMA (child’s investing account).

If the former idea is too involved or the money is not available for buying actual shares of companies, consider offering your child a “matching program” when they invest in the “Parent Company”. In the same way, consider offering your child interest (growth) for leaving their savings with you. They may need a greater incentive to understand the concept and value of having their money grow. Based on the child’s age, show them a toy that costs $1 and a toy that costs $10. They could spend their $1 weekly allowance collecting numerous low cost and low value toys, or they could save and potentially even grow their dollars to achieve a valuable toy more quickly. This would help provide the incentive to invest those dollars rather than spend them or even save them.

Lastly, teach the rule of 72. An investment that grows 7% annually will double in just over 10 years (72/7=10.2). An investment that grows by 10% annually will double in just over 7 years (72/10=7.2).

The discipline of spending

A great place to start is needs and wants. How much should be allocated to needs and what is left for wants. A rule of thumb is 50% for needs and 20% for wants. Without a credit card line, this is much easier to do when working on a cash basis. Until kids are old enough to have expenses like cell phone, auto insurance, gas, it will be difficult to break out needs versus wants. Until then, spending will be all one category at 70%. Once the child is a high schooler, they will experience more reasoning between needs and wants. What is left over is available for “fun money”.

It will be important to discuss the topic of credit versus debit as credit cards are a form of debt and borrowing from an institution will have numerous negative effects on saving and investing.

Another concept to teach when considering spending is discounts and coupons. When paying less for a specific item, you have more left over for other items or for saving, investing, or giving. One of the best places to teach this is looking at a specific product at the grocery store (candy bars!) and comparing prices, those on sale and those that are not and the impact of spending less to keep more.

The compounding benefits of financial literacy

Financial literacy, like investing, has compounding benefits especially when starting young. It is invaluable to model and have conversations around money with your children. No need for perfection, but the goal is to make progress and provide opportunities to learn.

This article was inspired from a presentation by Mac Gardner, CFP®, author of “The Four Money Bears”.