Why Portland Area Executives Are Getting Hit at Tax Time and What to Do About It

As a leader at your company, you are provided a comprehensive range of benefits that help achieve your financial and retirement goals. However, things can go awry at tax time. The newer Metro and Multnomah County taxes, in addition to regular Federal and Oregon taxes, are becoming an increasing burden for executives to navigate.

By implementing a proactive forward-looking tax strategy and payment plan, company leaders have a significant opportunity to improve their financial situation, relieve stress related to taxes, and reduce unwanted April surprises!

In this article, we’ll examine a few of the biggest reasons you could get hit with an unexpected tax bill and ways to navigate it differently.

Tax hit #1: Limiting your withholdings on supplemental pay

Many sources of compensation beyond salary (such as PSP, LTIP/PSU vests, RSU vests, and stock option exercises) are taxed as “supplemental pay.” This comes with a fixed tax withholding percentage, regardless of your tax bracket or withholding elections on your base salary. For example, the fixed withholding rates set by the government on supplemental pay is 22% Federal and 8% Oregon. The reality is most executives are in a much higher income tax bracket, sometimes as much as 17% higher than the amount withheld. This discrepancy leaves a significant gap in the amount of taxes that should have been withheld versus the actual amount that was withheld.

As an example, Charlotte an executive has $50K of RSUs that vested on September 1st. With all her income sources (salary, PSP, LTIP/PSU, RSUs) her total taxable income is $400K. The taxes automatically withheld on the $50K vested RSUs would be about $15K (22% Federal + 8% Oregon). However, her total income puts her in the 35% Federal tax bracket + roughly 10% Oregon bracket. This makes the withholding on her RSUs about $7,500 short ($50K x 15% short).

To get this paid in, she could use Quarterly Estimated Tax vouchers to submit the underpaid tax to the IRS and Oregon. Or, depending on her overall tax situation, she may be able to wait and pay the balance due with her tax return in April without incurring underpayment penalties and interest – although this determination may require a tax professional to run a detailed tax projection. For many people, being hit with a large bill all at once in April may not feel great and they may opt for Quarterly Estimated Payments instead.

If Charlotte doesn’t realize that her withholding was short until she files her tax return next April, she could face yet another surprise – 7 months of underpayment interest and penalties. Depending on her overall tax picture, the IRS and Oregon may have been accruing this since September. Yet another unwanted surprise for Charlotte.

Tax hit #2: Not withholding enough (or at all) for Multnomah County’s “Preschool for All” tax

The Preschool for All tax is 1.5% on taxable income over $125,000 for individuals or $200,000 for joint filers, with an additional 1.5% on taxable income over $250,000 for individuals or $400,000 for joint filers. The rate is currently scheduled to increase by 0.8% in future years. If you live or work in Multnomah County, you are likely subject to the “Preschool for All” tax that started in 2021.

Unfortunately, your company might not use payroll withholding to cover this tax, in which case you would be responsible to fully submit this tax on your own. Multnomah County expects these payments to be received quarterly to avoid interest and penalties. This can be submitted using vouchers or paying online.

We often see the most challenges for residents of Multnomah County who travel outside the county boundaries to work for an employer that does not currently have Preschool tax withholding options. Determining how much to pay and navigating this alone can be stressful. And for any late or underpaid tax, the county is quick to send notices in the mail. To reduce this headache, we recommend finding trusted advisors or tax professionals to serve as a guide to help you navigate complexities throughout the year.

Tax hit #3: A lack of coordination on how much to withhold for the Metro tax if you and your spouse both work

The Metro Supportive Housing Services tax (a.k.a. the Homeless tax) also began in 2021. It is a 1% tax on applicable income over $125,000 for single filers or $200,000 for joint filers. If you don’t know whether your residence or your workplace is located within the Metro, you can look up the address here: Metro Link.

The challenges described above for the Preschool tax are similar for the Metro tax. Additional issues arise for families when each spouse works at a different company, and we see this frequently because the Metro area is larger. The income threshold for this tax is based on total household income. Since the spouses’ two different employers likely do not communicate with each other, there can be significant over or under withholding of these local taxes.

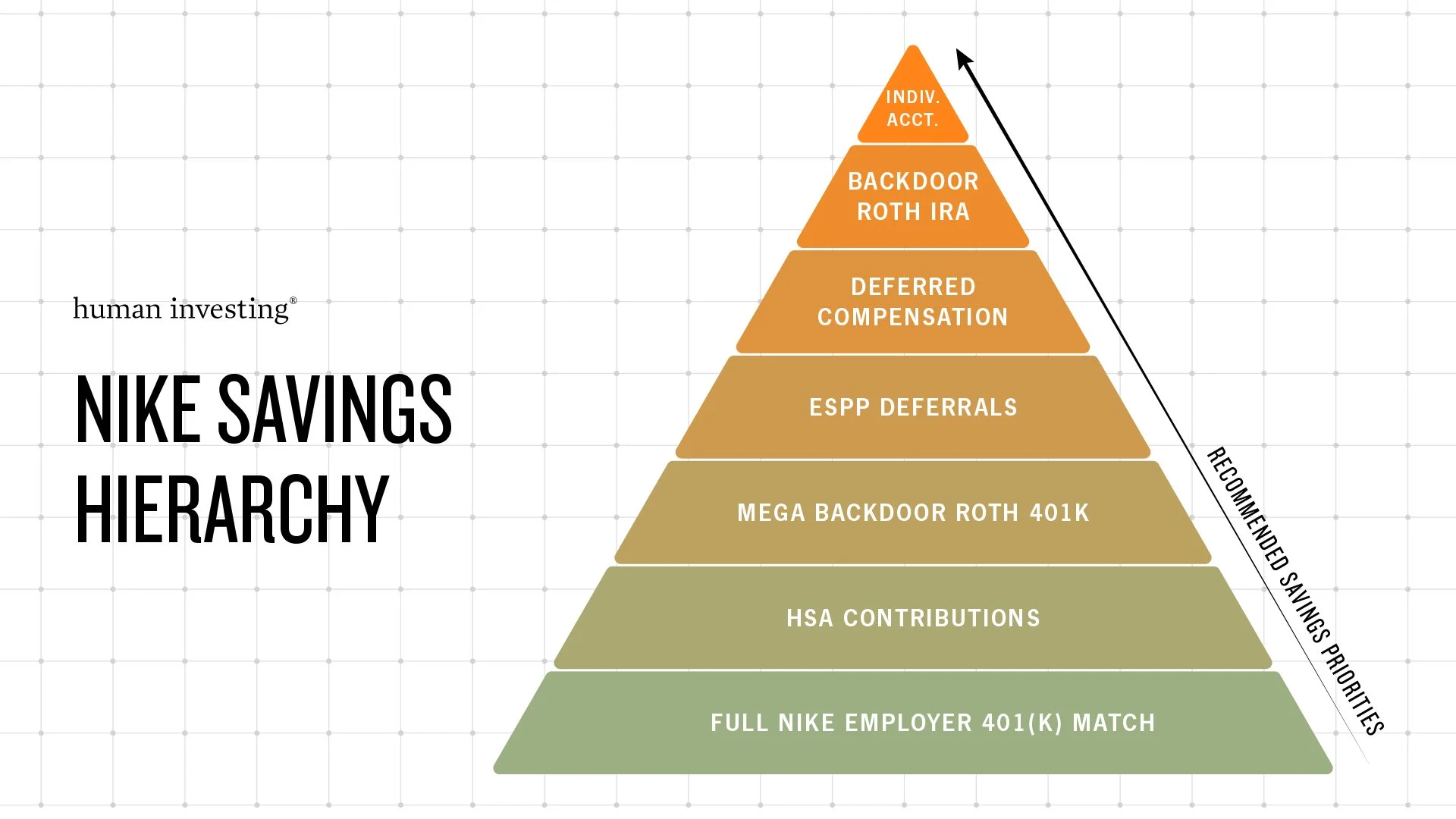

For example, Nike is located within the Metro boundary. If a Nike executive has income of $400K, Nike will start to withhold Metro tax once the executive’s income for the year is over $200K. Let’s say their spouse earns $90K by working for a different company, ABC Co., located across town but still within the Metro. Since this $90K alone is under the threshold, ABC Co. does not automatically withhold Metro tax. However, we know the total household income of $490K is over the threshold, which means all of the ABC Co. income is subject to Metro tax too. You see how this can create an issue? Unless the spouse realizes this and works with ABC Co.’s HR department to turn on withholding or diligently submits quarterly payments to the Metro on their own, the family may discover a balance of tax, penalties, and interest to pay in March/April right around a spring break vacation with their kids. Not fun!

In short, if you live or work in the Metro boundaries, it is important to be aware of the withholding options that your employer provides, and to be certain you are opted in or out accordingly.

Tax hit #4: Incorrectly reporting stock transactions and the complexity that comes with it

Up to this point, we’ve discussed withholdings on your salary and benefits. What about company stock that you own and decide to sell – what can go wrong there?

When you sell company stock (whether you’re still at the company or have moved on), it is reported to you and to the IRS by the custodian (i.e. Fidelity, Schwab, Computershare) on a Form 1099. On this form, the custodian clearly reports the sale date, quantity, sales price, and name of the company’s stock that was sold. What is not so clear is the basis – the portion of sales proceeds that is not taxable because it has already been taxed on your W-2.

If the stock was acquired as part of your employee benefits package, this information is often buried within dozens of pages in the Form 1099. And these pages can be detailed, complex and confusing to read - especially as each custodian has a different template and the layout can change from year to year. We recommend seeking the help of a professional if you are unsure about your basis or how to report it. An experienced tax preparer sees MANY of these forms each season. They know where to look to find the basis of the company stock you sell, and how to translate that information accurately onto your tax return.

Without reporting the basis, or reporting it incorrectly, your taxable income could potentially be overstated significantly and you may accidentally pay more money to the IRS than is actually due. Fixing this after your tax return has been filed can require a time consuming process of preparing an amended return and waiting for the government to return your money. If you suspect you overpaid your taxes, you can always reach out to a tax professional to review your tax return. CPAs within our firm often provide this review to clients throughout the year as part of our financial planning services.

While tax is a complex subject, it is only a piece of your unique financial picture. Planning appropriately for taxes should be done cooperatively with other parts of your financial plan, such as cash flow, retirement and estate planning. Done right, they’ll fit together like a perfect puzzle.

Want to minimize the tax headache? A few Actions you can take now

Action #1: Bring in experienced tax professionals.

Tax professionals can work with you to run “tax projections” to track how much you need to pay and monitor your April balance. These tax projections can be done any time throughout the year and can be refined near year-end to give you peace of mind and limit unwanted surprises.

If you’re looking for tax savings now or in retirement, we highly recommend proactive tax planning. A professional who is well-versed in your company’s benefits can use your tax projection to provide customized strategies to minimize your tax liabilities.

Action #2: Talk with your financial planner.

We know that for many company executives, setting aside additional tax payments from your monthly household cash flow can become stressful, especially since the amounts can be so inconsistent. If you’re feeling that stress, tell your financial planner – they’ll want to know so they can help you navigate it well and feel more confident going forward.

One strategy we may suggest is the “Pay as You Receive” method, which calculates an estimated amount of taxes due from each type of supplemental income when it hits your bank account. Making tax payments at the time you receive the income- while you have the funds to do it- will leave your monthly cash flow separate and unaffected.

These estimated tax payments, when combined with your payroll withholding, should be equal to your anticipated tax bracket for the calendar year. This approach helps ensure that your total payment to the IRS, Oregon, Multnomah County, and Metro aligns with your overall tax obligations.

Action #3: Find a team that has BOTH!

It is important to note that any tax payment and mitigation strategies should be part of a comprehensive financial plan that is tailored to your specific financial situation. If you’re considering a firm that can look at your full financial picture, we’d love to help. At our Lake Oswego office, our team has licensed CERTIFIED FINANCIAL PLANNER® professionals and Certified Public Accountants, and we constantly share knowledge with one another.

We’re here to talk you through local, state, and federal complexities and we want to help you get things right the first time. Our mission is to serve you faithfully and be there to guide you through your benefits packages as you advance in your career or make a move.

If you have questions about how to set up a proactive forward-looking tax strategy, please contact our team to learn more.

Disclosures: The information provided in this communication is for informational and educational purposes only and should not be construed as investment advice, a recommendation, or an offer to buy or sell any securities. Market conditions can change at any time, and there is no assurance that any investment strategy will be successful. Investing involves risk, including the potential loss of principal. Past performance is not indicative of future results.

Diversification does not guarantee a profit or protect against a loss in declining markets. Asset allocation and portfolio strategies do not ensure a profit or guarantee against loss.

This material is not intended to provide, and should not be relied upon for, tax advice. Please consult your tax advisor regarding your specific situation.

Scenarios discussed are hypothetical and for illustrative purposes only. They do not represent actual clients or outcomes and should not be interpreted as guarantees of future results.

The opinions expressed in this communication reflect our best judgment at the time of publication and are subject to change without notice. Any references to specific securities, asset classes, or financial strategies are for illustrative purposes only and should not be considered individualized recommendations.

Human Investing is a SEC Registered Investment Adviser. Registration as an investment adviser does not imply any level of skill or training and does not constitute an endorsement by the Commission. Please consult with your financial advisor to determine the appropriateness of any investment strategy based on your individual circumstances.