Quarterly Economic Update 2026: A Visual Guide to Long-Term Investing

The media offers plenty of reasons to worry. The ongoing conflict in the Middle East, AI rendering human workers obsolete, rising energy costs, the list goes on and on. If you’re investing for the long run, know that headlines will consistently try to pull you off course. Remember why you’re investing: You’re aiming to grow your dollars today to ensure you can maintain (or even grow) your spending power in the future. The rollercoaster of owning equities is rewarded with greater returns and spending power in the future.

Understanding the risk and reward of investing can be challenging. The finance industry likes to use terms like Beta or Standard Deviation. While these are statistically sound measures, most people would be hard-pressed to provide a clean and clear definition of what they mean, or how they’re calculated. Even most advisors would struggle to provide accurate definitions on the spot.

We try to communicate in Human terms with our clients, and we’ve built some charts and graphs to help communicate that. Given the current concerns and headlines, I think this is a great time to showcase some of our favorite graphs.

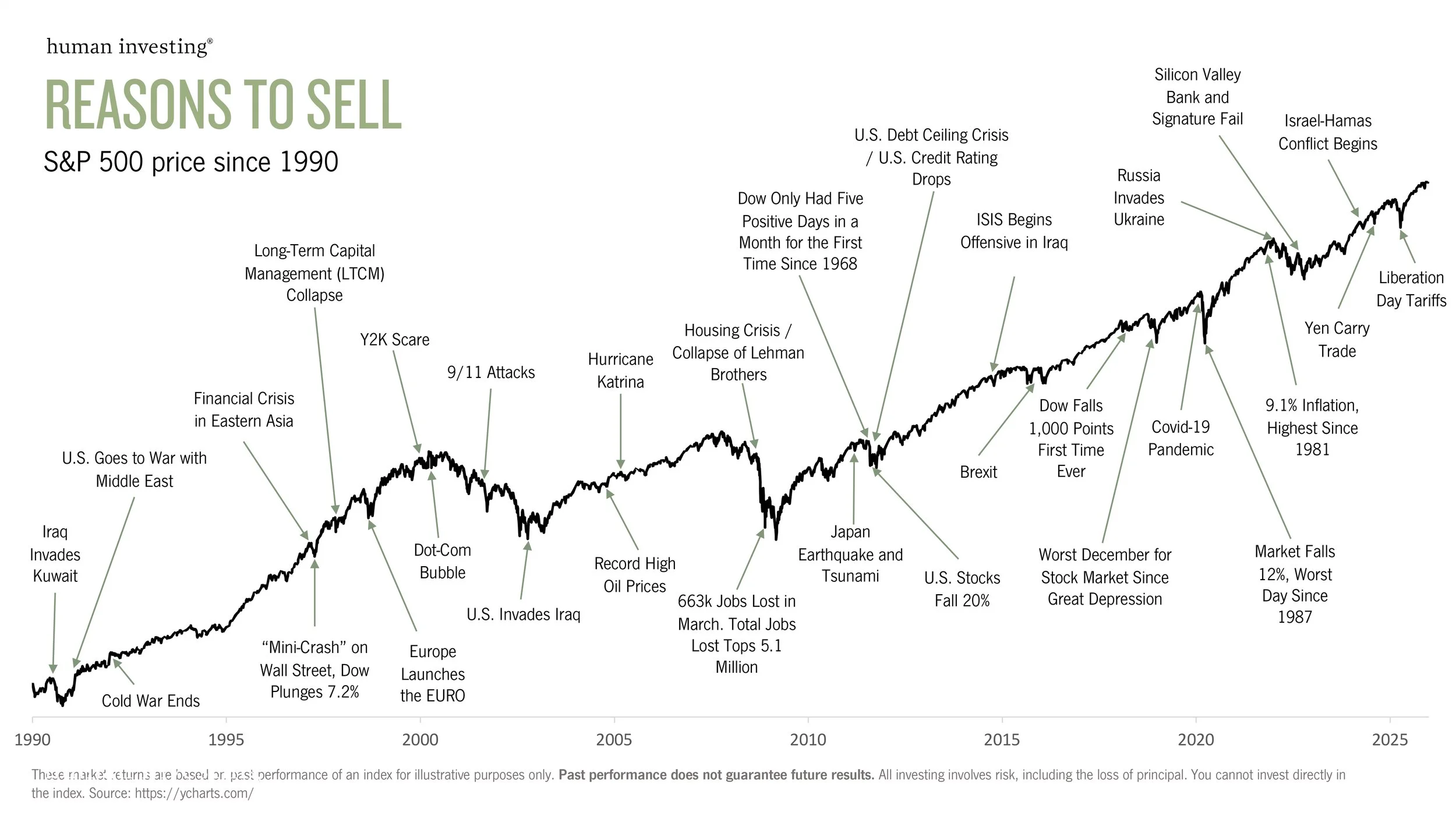

This is one of our favorite graphs. It's always easier to see that yesterday's worries weren't as scary once they're in the rearview mirror. Even through the Dot-Com bubble bursting, the 07-08 global financial crisis, and the COVID-19 global pandemic, stocks have risen. While we may not know the length or extent of a given market downturn, we do know companies have historically navigated challenges and delivered positive returns to long-term investors. We expect that resiliency to continue.

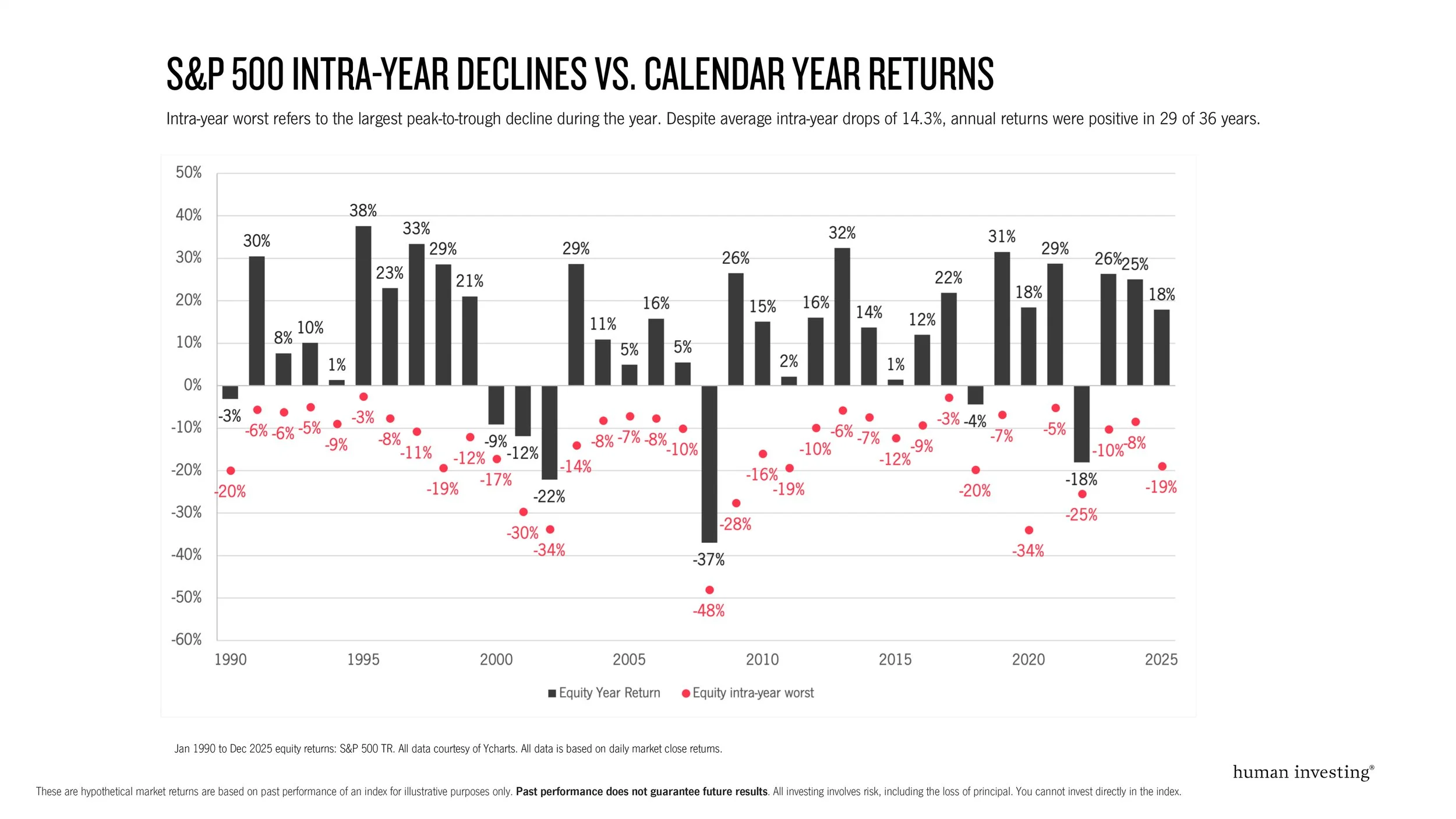

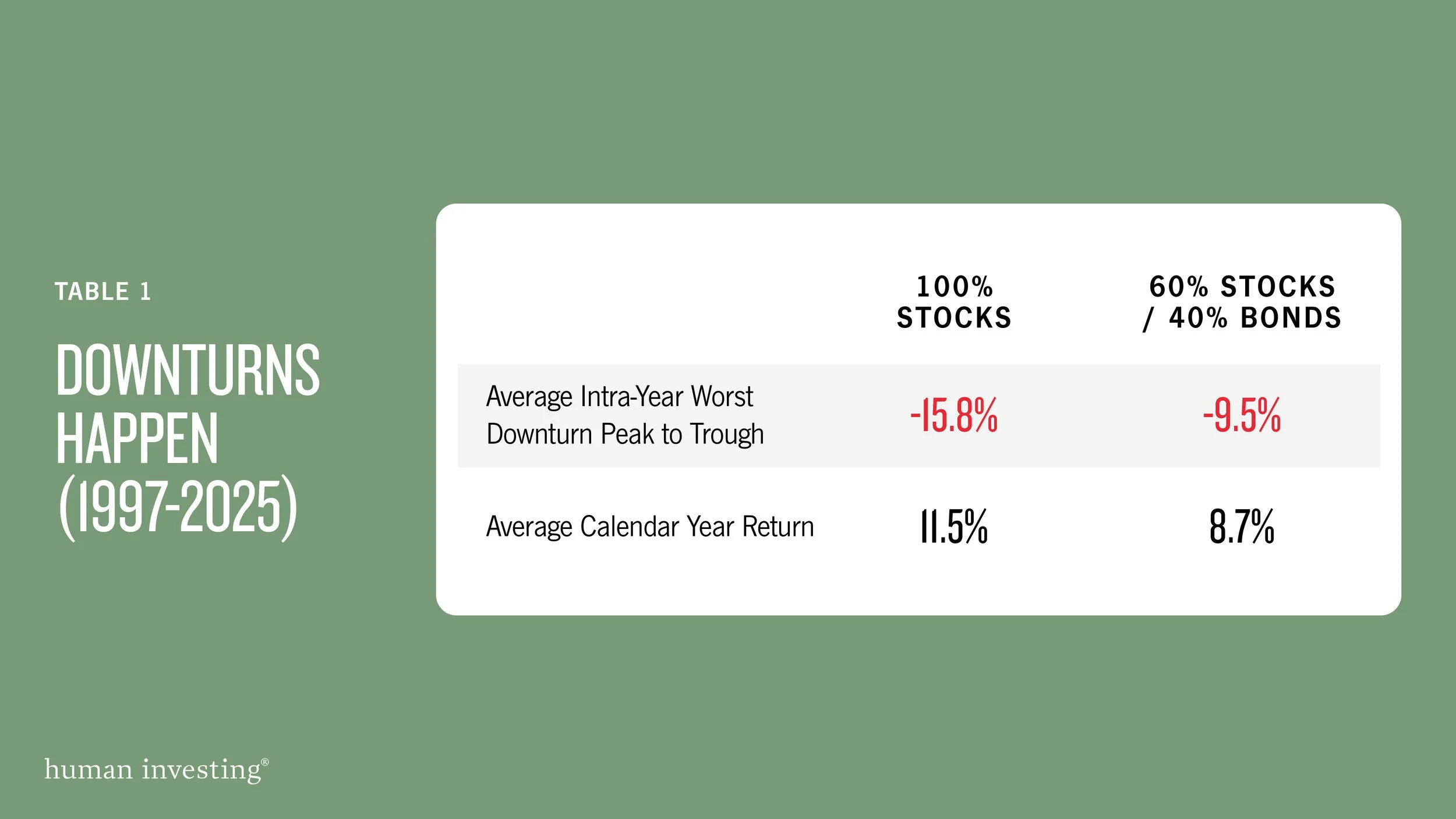

Introducing Intra-Year Declines

Markets rarely move in a straight line. Even in strong years, there’s almost always at least one significant drop along the way — what we call an intra-year decline. It measures how far the market fell from its highest point before it started recovering. As you can see in the chart below, intra-year declines have occurred every single year in the S&P 500 since 1990.

As I’ve written previously, the stock market is biased towards delivering positive returns. Most calendar years, stocks are up. This graph speaks to the lived experience of investors: every year has a downturn, no exceptions. I’m sure each downturn felt reasonable but worried investors at the time. No investor from 1990-2025 was immune from seeing their portfolio go down. Those who stuck with it saw positive returns in over 80% of those years.

Even amidst recent headlines, the market’s behavior has been typical. The S&P 500 dropped roughly 9% from its January peak to its March low. This is well within the normal range of market volatility where intra-year declines of 10% or more are common.

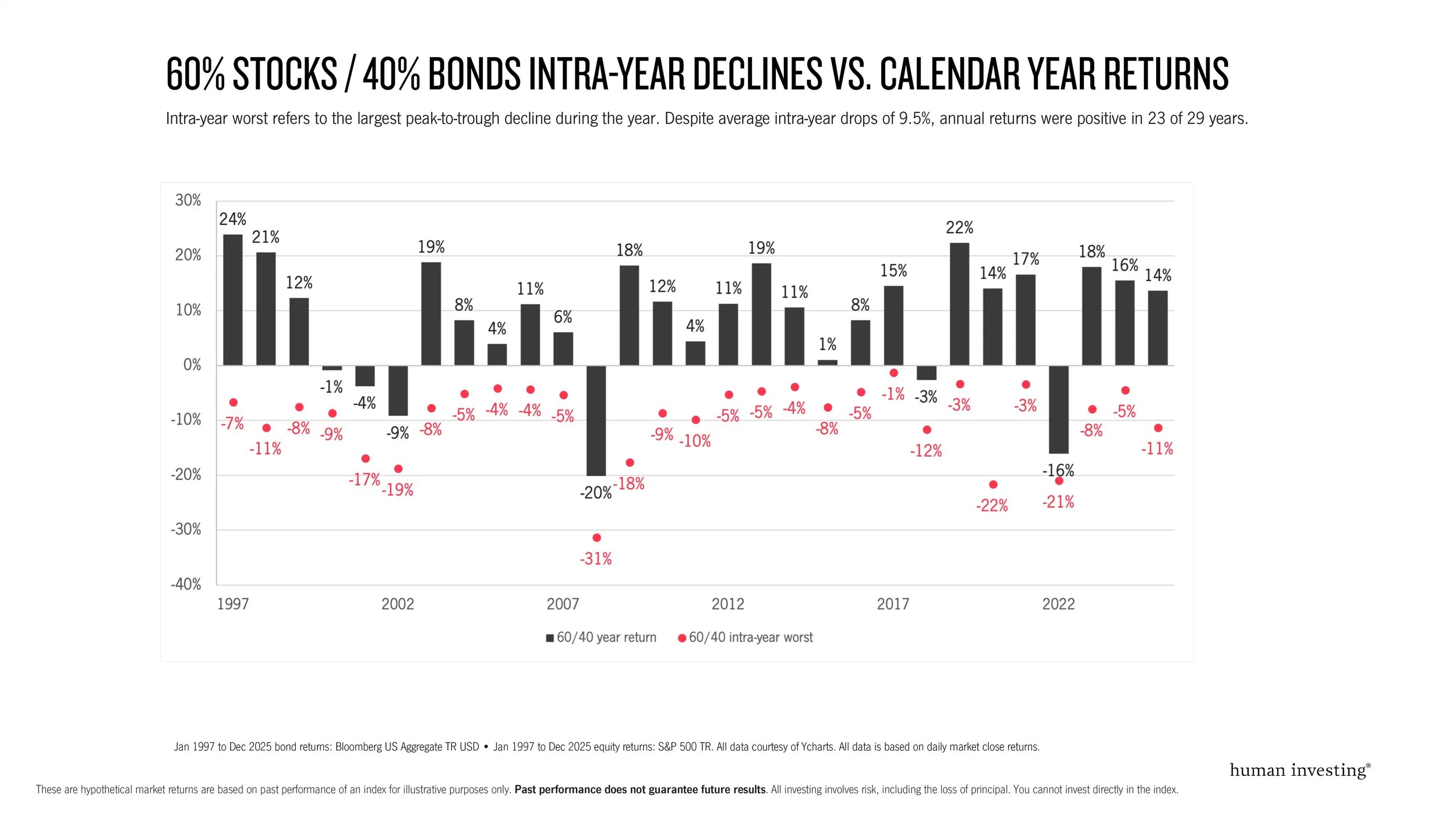

Most investors don’t own 100% equities, so it’s important to understand how introducing bonds can reduce risk. 60% equity and 40% bonds (60/40) is a common allocation because it tends to be a sweet spot between positioning your portfolio to grow and reducing risk enough to weather the volatility. Knowing where your asset allocation should be and when is an important, personal, complicated conversation that should involve a financial planner.

As you can see, while shifting from stocks to bonds doesn’t eliminate downturns, it certainly lessens them. Higher returns tend to come with more ups and downs, while smoother rides usually mean lower long-term growth. There’s no perfectly safe way to grow your dollars faster than inflation, so risk is always going to be part of your investment strategy. The key is finding the right balance between how much risk you’re comfortable with and how much risk you actually need to take to reach your financial goals.

Making plans that last

Anytime we’re designing a portfolio at Human Investing, we’re trying to make decisions we’d be okay with over the timeframe that matters for YOUR goals. That doesn’t mean we don’t revisit or adjust, but we’re not trying to make short-term tactical moves. We know outsmarting the market is incredibly difficult to achieve. We’re planning for our clients’ lifetime, not the next 6 months. We want to ensure our clients are positioned in a way where they are capturing the growth necessary to reach their financial goals, while having enough safety they don’t panic because of a temporary downturn.

No matter how you think about risk, there are a few enduring truths. Stocks are a volatile investment, but they’ve historically been a great growth engine in the long run. Whatever headline or concern today will feel much smaller in the rearview mirror.

Your financial plan and investments are meant to serve you over your entire life, not the current news cycle. There will be times when it makes sense to revisit your allocation, especially when your personal circumstances change. Those decisions should be driven by your goals, not the headline of the week.

We’re always happy to have conversations to help you understand how your allocation is set to fit your needs. Call us at 503-905-3100, or email hi@humaninvesting.com.

Disclosure: This material is provided for informational and educational purposes only. It should not be construed as investment, legal, or tax advice, nor does it constitute a recommendation or solicitation to buy or sell any security. Any market commentary, forward-looking statements, projections, or return expectations discussed are based on assumptions and current information and are subject to change. There is no guarantee that these views will be realized. Investors should consult with a qualified financial professional before making any investment decisions. There is no guarantee that any investment strategy will achieve its objectives, and investing involves risk, including the potential loss of principal. References to market indexes (including the S&P 500 and blended stock/bond allocations) are for illustrative purposes only, are unmanaged, and do not reflect the performance of any specific investment or client account. Index returns do not reflect the deduction of fees or expenses. Historical returns, projections, or economic conditions are illustrative only and should not be considered indicative of future results. Past performance is not a guarantee of future outcomes. Asset allocation and diversification strategies do not ensure a profit or protect against loss. Advisory services offered through Human Investing, an SEC-registered investment adviser.