A transplant to the Northwest, I recently developed a penchant for hiking. It’s necessary to point out the fact that I’m not a native of the Pacific Northwest, if only to highlight the amount of wonder that I experience every time I venture beyond the city limits. For me, every step reveals something new and exciting that I never encountered in the Midwest. Hiking in Ohio is quite literally a walk in the park compared to the trails out here, and I’ve learned the importance of being organized and prepared. Not long ago, I was packing for a trip to Mount St. Helens, going through my checklist, and my thoughts turned to retirement planning. In part because I knew that I had this blog to write once I returned, but also because I’m actually passionate about the subject. Much like hiking, planning for retirement requires some forethought and strategy. With that in mind, here are my top three hiking/retirement planning tips!

Don’t lose sight of the trail while hunting for Sasquatch...

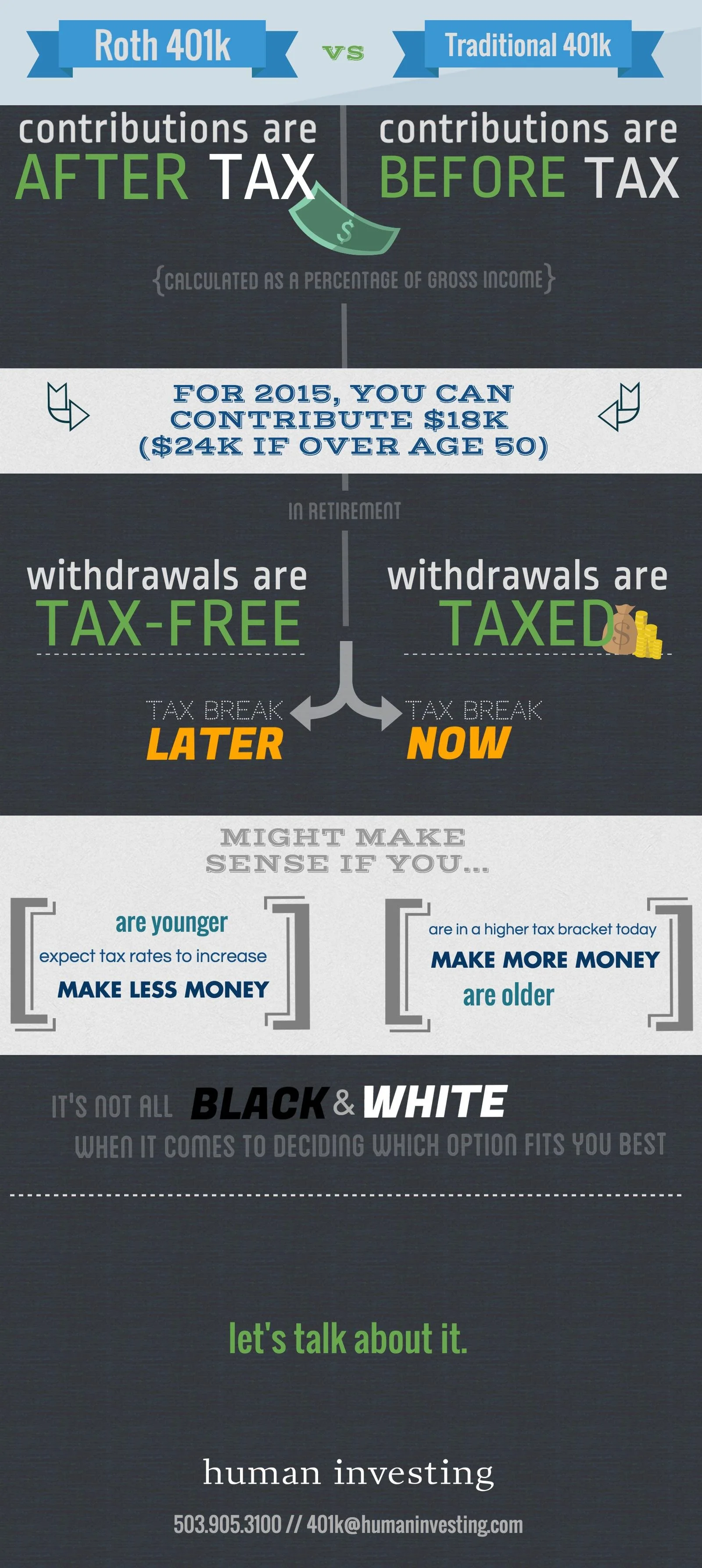

We’re often asked, “what is the best investment?” This is a simple question that warrants a complicated answer because factors like age, risk tolerance, and estimated retirement date can all influence an individual’s investment strategy.

The Putnam Institute completed a study in 2012 that showed the impact of selecting the top performing investments quarter over quarter (labeled the “crystal ball strategy”) vs. increasing your savings rate. The study revealed that while the crystal ball strategy yielded a higher account balance than the base case, a 1% increase in savings rate “had a wealth accumulation impact 30% larger than the crystal ball fund selection strategy”. In other words, we can’t always control selecting the “best” fund, but we can control how much we save.

I’m not saying that we should stop trying to invest well, (or that we should stop hunting for Sasquatch for that matter). I am suggesting that focusing too much on finding the best investments, can distract from other facets of retirement planning that are just as important.

Quality gear is worth the extra expense...

The retirement planning side of this tip is that saving more now, will greatly impact your savings in the long run. This is something that we all know, but it can be difficult to commit to increasing your savings rate until you see the actual numbers. For example, saving in your 20’s and 30’s has a greater impact on your lifetime savings than saving later in life. Due to, compounding returns, someone who saves $4,000 a year from age 30 to age 40 will end up with a greater balance at 65 than someone saving $4,000 a year from 40- 65, assuming a 7% rate of return. I know that statistic seems hard to believe, but check it out, it’s true!

There’s always another mountain...

It’s important to remember that the day you retire isn’t the end of your journey. A 2012 CDC study reported that life expectancy is 78.8 years, which is up from 70.8 in 1970. The point being, often times when transitioning into retirement, retirees feel the need to preserve their “nest egg”. When in reality taxes, inflation, and health care expenses are eating away at their savings. By recognizing the dual purpose of retirement accounts; providing cash flow and growing for the future, you can climb the mountain right in front of you while also planing for the ones on the horizon.

Have questions about the transition from retirement savings to retirement income? We can help with that!

As far as the hiking goes, it’s going to take a long time for me to see all there is to see around the Pacific Northwest. Personally, Dog Mountain (seen on the right) is one of my favorites.

You should also note that if you’re hiking in the rain, “windbreaker” does not equal “rain jacket.” I may or may not have made that mistake.

Call or email us at 503-905-3100 or 401k@humaninvesting.com