Tax season creates stress for a lot of people. It often starts with tracking down documents from multiple places, turns into uncertainty about what might be missing, and ends with concern about an unexpected tax bill at exactly the wrong time.

As a financial advisor at a firm that prepares taxes in house, I get a unique view behind the scenes. Each year, I see which situations go smoothly and which ones lead to stress, surprises, and last‑minute scrambling.

With another tax season behind us, here are five ways to make the next one more predictable and far less stressful.

1) Eliminate any surprises

One of the biggest drivers of tax stress is uncertainty.

The best way to create more certainty is to complete Tax Planning Projections during the prior year. Not only do they help identify tax‑saving opportunities while there is still time to act, but they also do something just as important, which is to set expectations and eliminate the surprises.

A good projection can answer questions like:

Will you owe or receive a refund and approximately how much will it be?

Do you need to set aside cash or plan where funds will come from?

Are there any estimated tax payments that I should make before the end of year to increase my deductions or minimize any interest or penalties?

When you understand the likely outcome ahead of time, April becomes about execution, instead of a scramble.

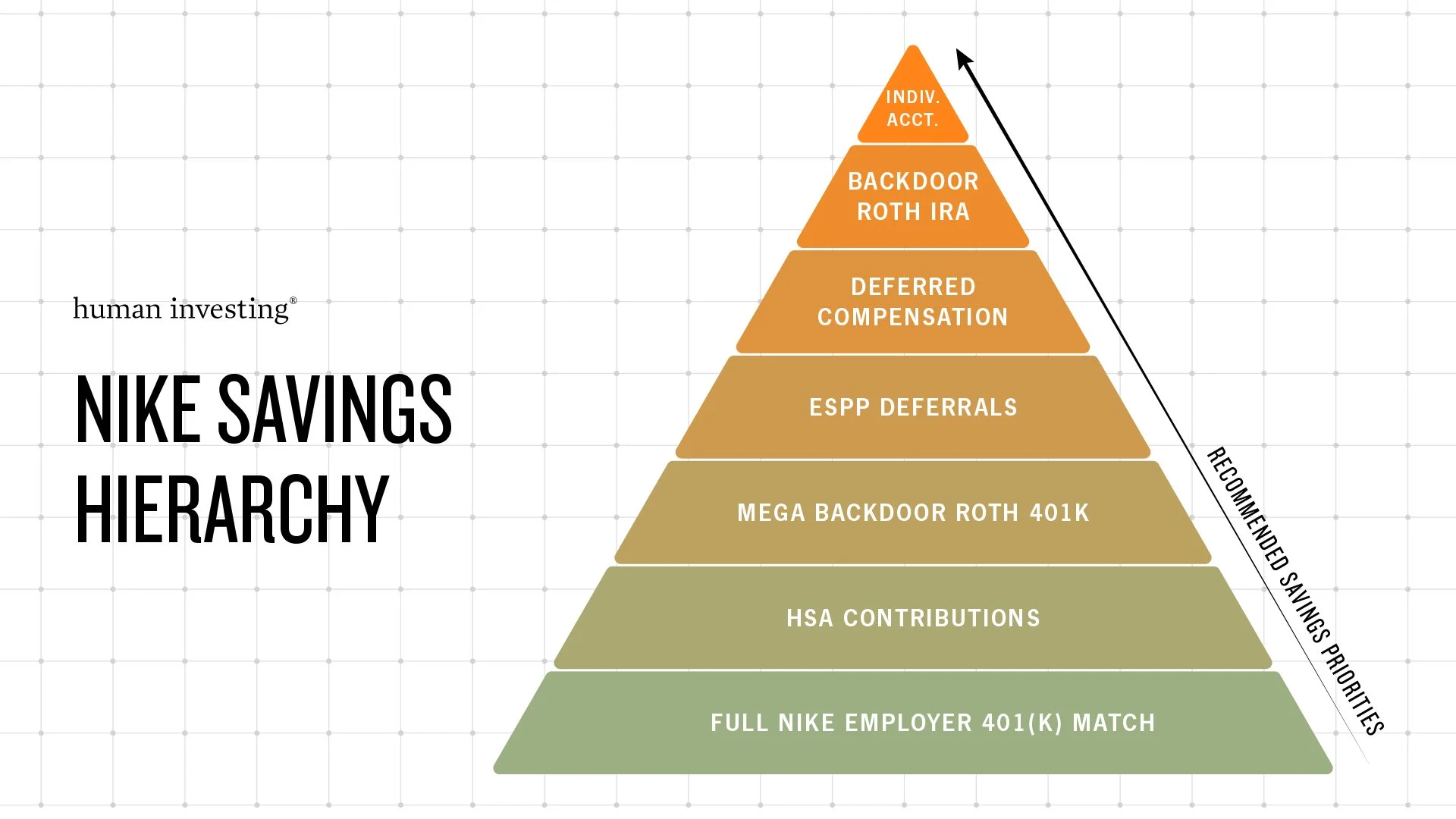

2) capture tax savings before the windows close

Capturing tax savings requires planning ahead of time and acting before specific deadlines. If you wait too long, you can miss out on the available opportunities.

Some strategies that often help clients reduce taxes now and in future years include:

Bunching charitable contributions using appreciated stock

Using Oregon tax credits funded with appreciated securities

Contributing to Deferred Compensation Plans

Roth conversions in lower‑income years

Strategically realizing capital gains in the 0 percent federal bracket

Tax loss harvesting

Managing income to qualify for ACA premium tax credits while avoiding Medicaid or the Oregon Health Plan

Funding self‑employed retirement accounts such as Solo 401(k)s and SEP IRAs

It is also easy to overlook contributions that can still be made right up until April 15:

Traditional or Roth IRA

Health Savings Accounts

Solo 401(k)s or SEP IRAs

Oregon 529 plan contributions

Planning ahead helps ensure these opportunities do not get missed simply because the deadline arrives quickly.

3) tackle your tax season in waves, not all at once

Tax season does not unfold evenly, it comes in waves so doing a small amount of work during each wave is helpful.

The First Wave: Late January through mid‑February is when the first wave of core documents arrives, including W‑2s, mortgage, and bank interest documents. I would recommend beginning to gather these documents as they arrive.

The Second + Final Wave: Mid-Late February: The second and typically last wave is Final investment 1099s for dividends, interest and capital gains from custodians like Schwab or Fidelity generally arrive later, and revisions are common. If you already have your first wave documents ready and submit those with your second wave of documents early enough you can often get to the front of the line for preparation.

As deadlines approach, CPAs and tax preparers experience capacity constraints. Submitting everything right before spring travel or just ahead of April 15 often means landing at the back of the line. If the goal is to wrap up your return earlier, having information ready before the surge makes a real difference.

Even if you plan to file an extension, these timelines still matter—an extension doesn’t eliminate penalties or interest if taxes aren’t paid on time.

4) make a proactive plan for your tax bill

Often the most stressful part of filing taxes is owing taxes. There can be a mental pain of parting with cash, which can be compounded by the question of where to get the funds. Is it going to come from your checking account, savings account or high yield savings account? If you don’t have enough cash, should you sell investments (which can create even more tax for future years) or should you take a temporary loan on your investment portfolio or your home via a home equity line of credit?

Other common challenges include:

Payment to one jurisdiction like the IRS while waiting for a refund from another like the state of Oregon.

Finding liquidity when funds are not readily available.

Making sure payments are applied to the correct tax year rather than misclassified as estimates for a different tax year.

Mistakes here can cause payments to be misapplied or returned, creating the frustrating experience of being told you never paid.

Having a professional help you determine the best funding source and even facilitating tax payments on your behalf can remove much of this complexity and significantly reduce the risk of error.

5) Remember that april 15th is two tax deadlines, not one

April 15th marks both the end of one tax year and the beginning of another deadline, which is Quarter 1 estimated taxes.

First‑quarter estimated tax payments are due on the same day. Many people default to a safe‑harbor approach based on the prior year’s income. This can help avoid penalties, but it is not always the most efficient option.

If last year’s income was unusually high, your estimates may require overpayment and effectively give the IRS an interest‑free loan.

If income is similar year to year, this can be an effective approach.

If income is rising, the safe harbor approach may keep you penalty free but still result in a large bill the following April that requires planning.

The right approach depends on where your income is headed in the next year, not just what tax software defaults to from the previous year.

These estimated taxes can add to the already painful tax bill due from the previous year, making proactive Tax Planning Projections even more important.

Bringing it all together

Most people will not execute all five of these steps perfectly, and that is okay. Even doing a few of them consistently can meaningfully reduce stress and improve outcomes.

Because these decisions span timing, tax strategy, cash management, and coordination, many people find greater value in having a partner help integrate the process rather than managing everything alone.

If you are evaluating tax preparation services, it is worth considering how well planning, execution, and follow‑through are connected, and whether you are realistically set up to do this on your own.

Tax strategy isn't a standalone service for us, it's woven into every financial plan we build. If you're ready to be more proactive about your taxes, our team at Human Investing is here to help.

Disclosure: This material is provided for informational and educational purposes only. It should not be construed as investment, legal, or tax advice, nor does it constitute a recommendation or solicitation to buy or sell any security. Any market commentary, forward-looking statements, projections, or return expectations discussed are based on assumptions and current information and are subject to change. There is no guarantee that these views will be realized. Investors should consult with a qualified financial professional before making any investment decisions. There is no guarantee that any investment strategy will achieve its objectives, and investing involves risk, including the potential loss of principal. References to market indexes (including the S&P 500 and blended stock/bond allocations) are for illustrative purposes only, are unmanaged, and do not reflect the performance of any specific investment or client account. Index returns do not reflect the deduction of fees or expenses. Historical returns, projections, or economic conditions are illustrative only and should not be considered indicative of future results. Past performance is not a guarantee of future outcomes. Asset allocation and diversification strategies do not ensure a profit or protect against loss. Advisory services offered through Human Investing, an SEC-registered investment adviser.