According to most research, although millennials are considered the most highly educated generation, we are the least informed when it comes to our financial decisions. Not only do we lack financial literacy, but pre COVID-19, 63% of millennials felt anxious when thinking about their financial situation, and 55% felt stressed when discussing their financial situation. I imagine COVID-19 has negatively impacted those figures even further.

There are many factors that affect our personal financial stress levels, but historically, the financial industry has felt inaccessible to those who lack financial literacy and/or feel insecure about their financial situation. How are we supposed to learn if we lack access to knowledge?

SAVINGS APPS TO SAVE THE DAY

I love the concept of savings apps, because it improves accessibility of investing and saving for a large population. Basically, if you have a smart phone and a few extra dollars, you can be a saver. A study conducted in 2019 found that individuals who used savings apps kept better track of their finances and were more resilient when faced with a financial shock. However, accessibility without education can be hazardous. So, here are two recommended savings apps that provide learning and saving opportunities.

Mint is a free app powered by INTUIT (think Turbo Tax) that houses all of your financial information in one place. Mint uses a holistic view and budgeting tools to find extra savings for you. Not only do they provide you with custom savings tips, but they also have a hub of resources, ranging from building a grocery budget to investing advice, so you can learn along the way!

Digit has the same philosophy as Mint: find savings within your current financial situation. With this philosophy, Digit analyzes your current income and expenses and then lets you know what you can afford to save. They invest your dollars in FDIC insured account using a portfolio based on your risk level and comfortability. You are also able to attach these savings to a specific goal – emergency savings, honeymoon, a doggo—you name it. There is a monthly cost of $5, but you do receive 1% annual bonus savings every three months.

NOT FEELING IT? FOLLOW THEIR SAVING PHILOSOPHIES

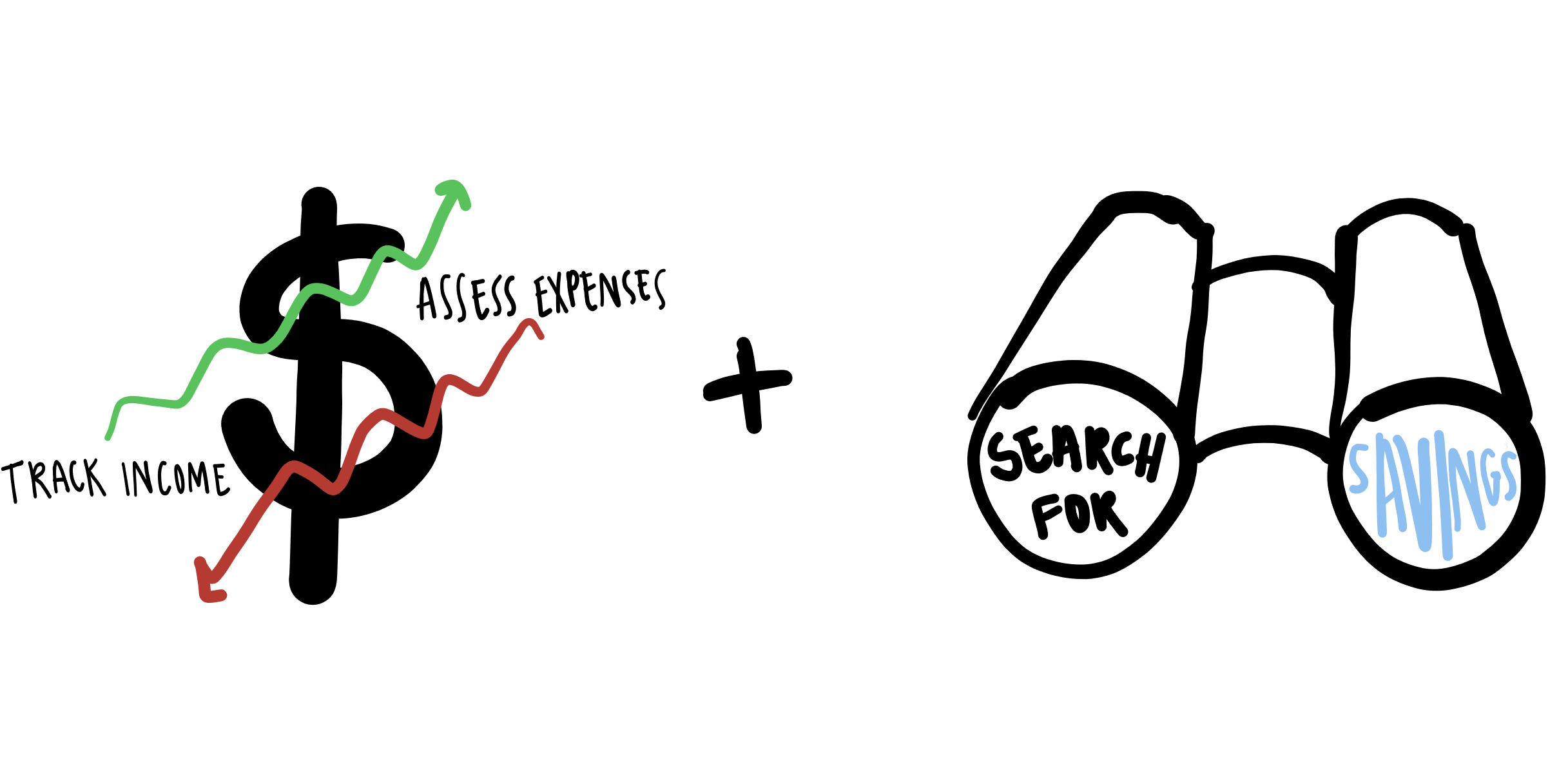

It’s okay if you don’t vibe with the savings app world. But if you do want a better grip on your finances, follow the philosophy behind the savings apps:

Keep track of your income.

Assess your spending habits.

See where you can save.

For me, that looks like walking past the gluten-free bakery every so often instead of into it (which is usually the case) and saving the extra $5. At the end of the month it can make a difference (Don’t believe me? See how much you can save by ditching your morning coffee here).

Finally, allow yourself to interact with financial resources without being too hard on yourself. The purpose of these apps is not to be a report card. The purpose is to empower you to make thoughtful decisions that will improve your financial health. If you have questions, check out our Financial Wellness Center or reach out! We are here for you.