It’s no secret that Nike has been going through a tough time with the recent rounds of layoffs. This can create concern and uneasiness around a Nike employee’s livelihood and how it may affect their financial picture. As we have been actively guiding our Nike clients through this season, we wanted to share things to consider if you were or will be impacted by these layoffs.

Understand Your Severance Package

Nike has a standard severance agreement and package that includes a one-time payout of cash based on your level and tenure at Nike. This can range from 4 weeks to 48 weeks of salary.

In addition, there is often a continuation of health insurance through COBRA that includes a subsidy of the cost for around 6 months. This provides some time to transition to a different health insurance plan if that is right for you.

If you have any accrued PTO that you haven’t used, this will be paid out to you in cash after officially leaving Nike. This is often extra cash that people are not expecting and can help create some comfort during an uncomfortable time.

Lastly, you may still be eligible for the PSP bonus paid out in August as long as you are still employed anytime in May (the last month of the Fiscal Year).

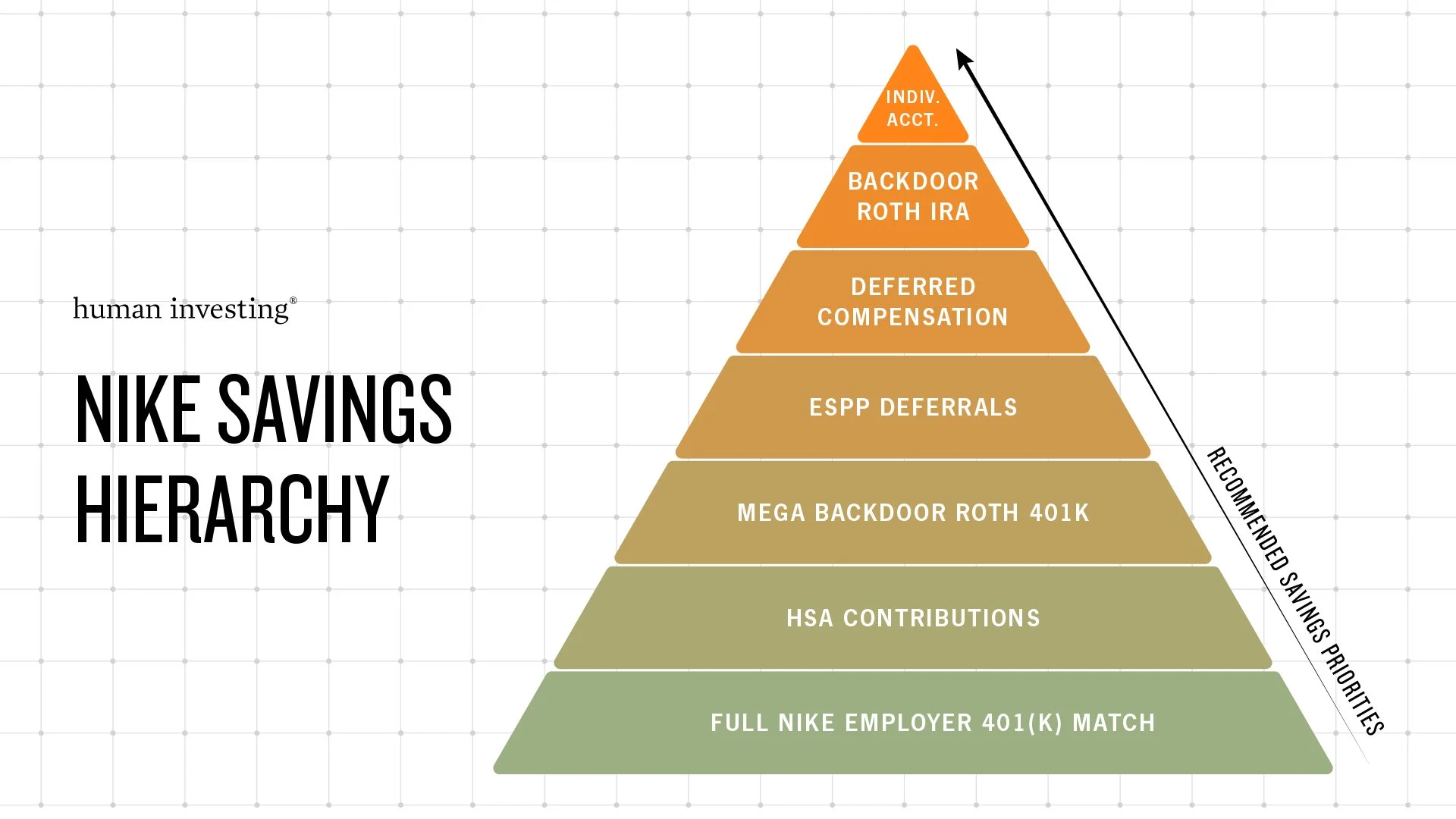

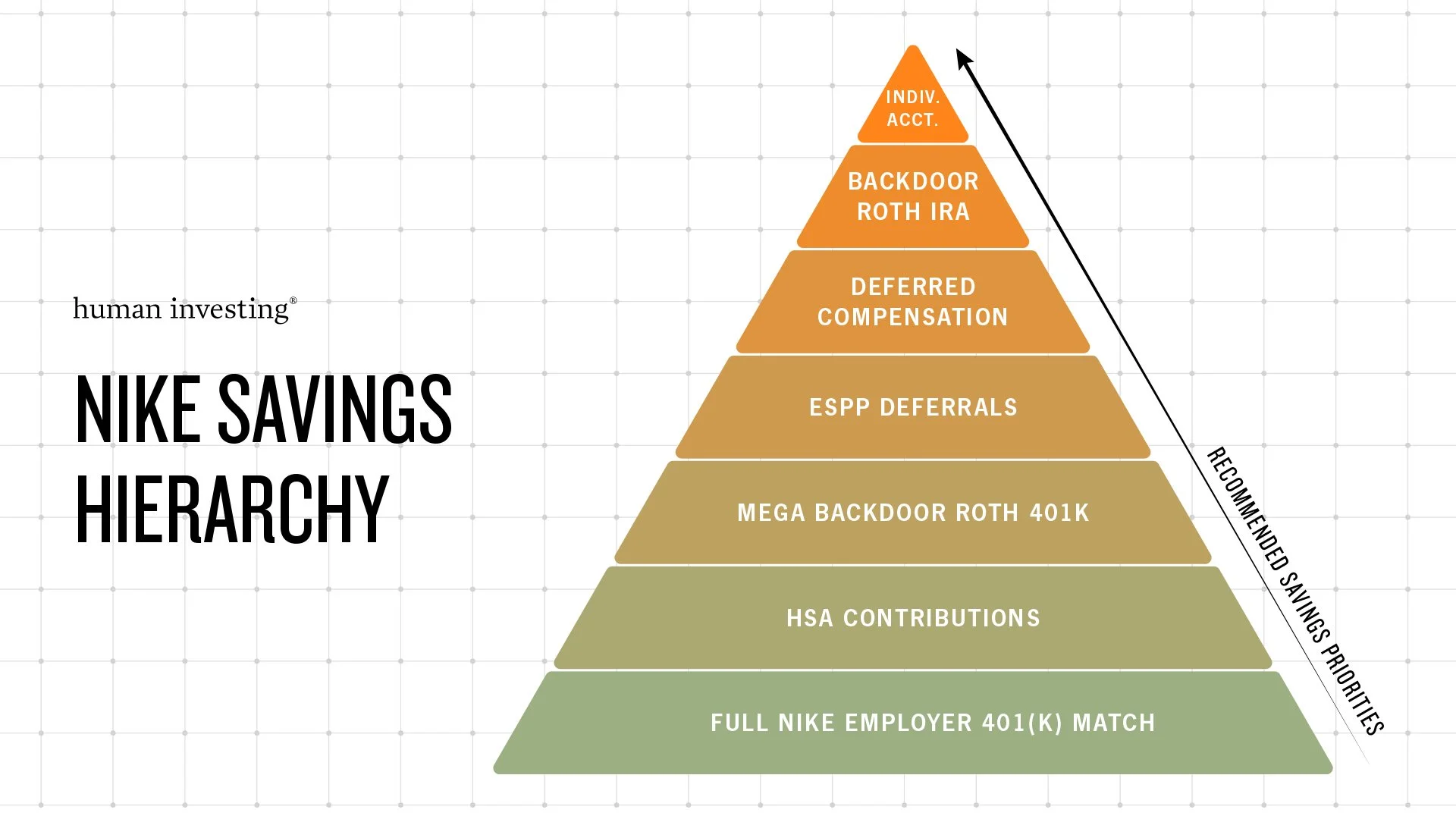

Create a Strategy for Deferred Comp Distributions

If you contributed to the Nike Deferred Compensation Plan, leaving Nike will typically trigger distributions according to the schedule you designated when enrolling. This can range from a one-time lump sum or installments over 5, 10, or 15 years. For some, this can be a way to supplement income. However, for others who don’t need the funds, these distributions can create a tax issue to strategize around. These payments are sent out quarterly, so if this is needed for cash flow you should plan accordingly.

Plan for your Stock Options and RSUs

Any vested but unexercised stock options typically need to be exercised within 90 days of leaving Nike, unless you qualify for the special retirement benefits at age 55 or age 60 (you keep unvested options and can sell for lesser of expiration or 4 years). At this time, you typically will lose any unvested options or RSUs.

During larger layoffs, there can be enhanced vesting of options and RSUs, where upcoming vests within a year will accelerate and vest. In addition, Nike can also provide you with more time to exercise your stock options like up to 1 year instead of 90 days. When Nike stock price is struggling like it is now, it makes your exercise decisions in a small window difficult. We would recommend working with your financial advisor to determine a defined strategy to maximize the benefit and minimize taxes.

Keep track of your PSUs and ESPP

Normally, you need to be employed at Nike at the vest date to receive your PSUs. In a situation of Reduction in workforce (larger layoffs), you can still receive any PSUs if the vesting date is within one year of termination.

Any ESPP that has been contributed but not purchased yet will be refunded to you. In addition, you have more control over your ESPP shares that you have purchased previously as these can be held as long as you want. This provides an opportunity to be patient and strategic on any sale of this stock.

Prepare to mitigate tax liability

All the benefits outlined above come with tax implications that are not always easy to see. These items can quickly add up to large amounts of taxable income, which can push your income into high tax brackets. In addition, the tax is often under-withheld (22% Federal and 8% State), which can lead to a significant tax bill in April if not accounted for properly.

Know your 401K options

This recommendation depends on each person’s situation. Nike has a strong investment fund lineup, and you should compare that to any other place that would replace it. However, leaving your 401(k) at Nike requires more activity and maintenance since it does not have an auto-rebalancing feature, which would periodically sell funds that drift from their target allocation. For example, if the large company stock fund was targeted at 60% and grew to 64%, you should periodically bring that back to the 60% target to maintain the proper risk/return mix. Another factor to consider is the desire to make Backdoor Roth IRA contributions if you have extra funds for retirement savings.

Support when transitioning into the next job

The cash you receive from benefits like severance, PTO payout, and stock sales can help provide some comfort to your situation. While you are in transition with your job, we recommend creating a system to feel like you are receiving a paycheck replacement with your cash to reduce anxiety and bring normalcy to your day-to-day financial life. An example of this system would be taking your net benefits payout and depositing it in a savings account, then setting up bi-weekly transfers to your checking account to simulate your paychecks.

All these considerations are tied to a person’s long-term financial plan. Through financial planning projections and scenario planning, you can help determine what the next job needs to look like to achieve your goals for retirement, kids’ education, and lifestyle. It can provide you with the information to know if you need a comparable compensation package to Nike or if you could take a job with lesser pay that could be more fun or less stressful.

Being laid off from any job often creates much uncertainty, stress, and concern. With the right preparation, planning, and advice, it can be a smoother transition, and you may end up in an even better place than where you started.

If you have questions about preparing for or navigating a current layoff at Nike, please feel free to contact us at nike@humaninvesting.com or schedule time with us below.