A combination of recent tax cuts, swelling government debt and changing political winds have many concerned about increases in future tax rates. This has created a growing interest in strategies that can lower and mitigate future income taxes. One such strategy is available and often missed by many Nike employees within their 401(k) plan, known as “Mega Backdoor Roth 401(k) contributions”. While the name often elicits laughter at first, it can in fact be a serious and tangible way to save on future income taxes.

What is the Nike Mega Backdoor Roth 401(k)?

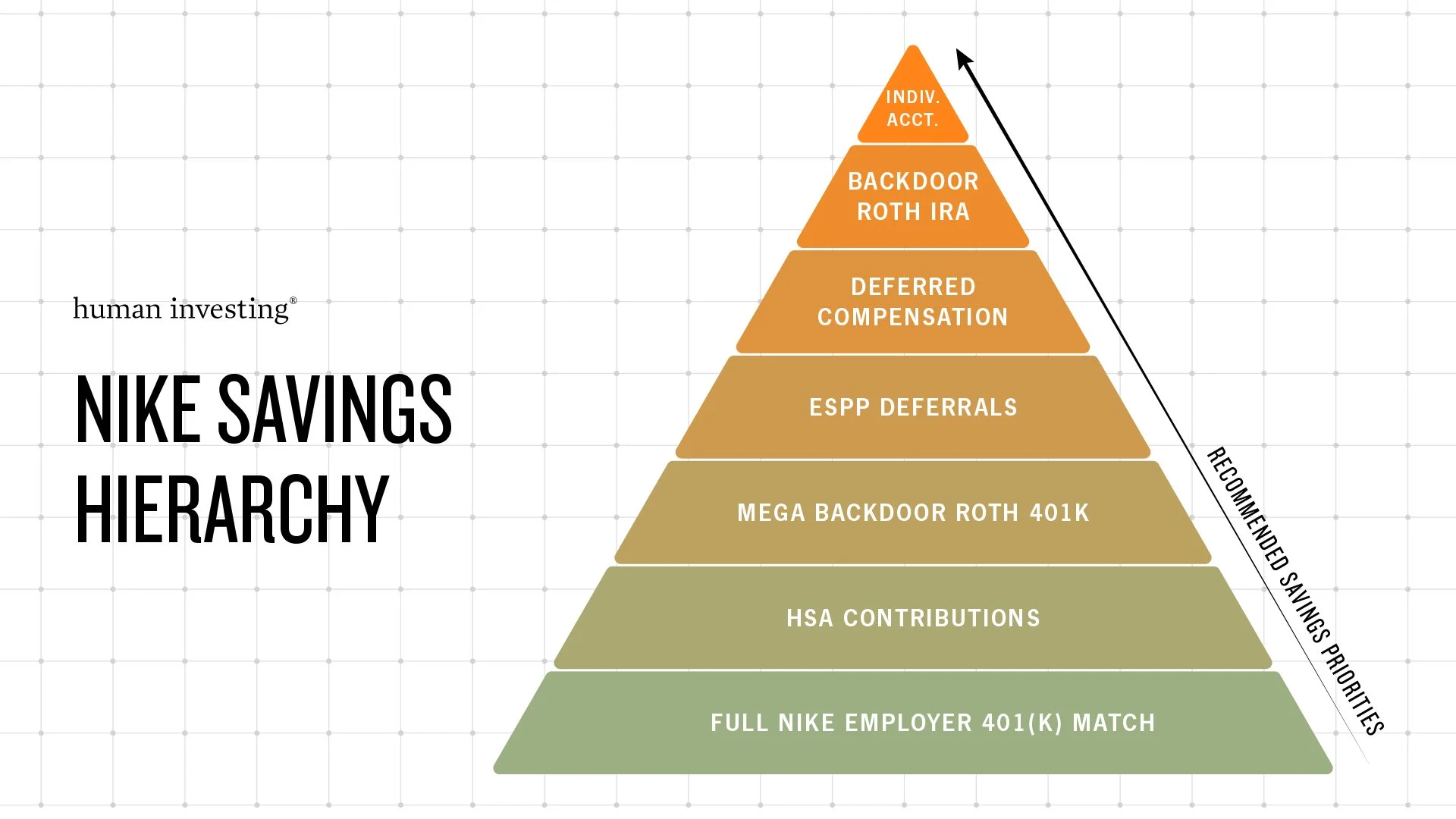

The Mega Backdoor Roth 401(k) provides the ability to make additional tax-advantaged contributions to the Nike 401(k) plan above and beyond the typical employee limits of $24,500, plus catch-up contributions of $8,000 for ages 50+ and an additional $3,250 for ages 60-63 (2026). The additional contributions are in the form of “after-tax” contributions of up to 3% of income. This applies to base salary and any PSP bonus. The total contribution amount will have a cap based on annual IRS limitations: $10,800 for 2026. The after-tax contributions can then be converted to Roth dollars within the plan, which allow them to grow tax-free and be distributed tax-free* in the future.

How to Execute the Strategy

The process starts by electing to make after-tax contributions within the Nike 401(k) plan of up to 3%. Once the after-tax contributions have been made, it is important to then convert these contributions into tax-free Roth funds* by periodically electing to do an “In-Plan Roth Conversion”. To complete the In-Plan Roth Conversion, the employee will need to call the Nike 401(k) phone line and make the request verbally. Be prepared to spend 10-15 minutes on the phone for the conversion process to be completed.

The In-Plan Roth Conversion is important because the growth of the after-tax contributions will become taxable as ordinary income upon distribution if the conversion is never completed. However, if you convert those funds into Roth dollars, then the future growth and distributions will be tax-free*. We recommend that the In-Plan Roth conversion be completed on a periodic basis to make sure that the funds are converted before any significant growth occurs. Any growth of the after-tax contributions at the time of this conversion will be taxable income, but if completed regularly, the growth and subsequent tax is typically minimal. Ideally the conversion would be completed after every payroll or monthly, but practically speaking, one to two times per year should be sufficient to effectively execute the strategy.

Is this Strategy Right for You?

Nike’s robust benefit options can leave many unsure of which savings plan is best for them. Whether it is 401(k) contributions, ESPP, Deferred Comp or Mega Backdoor 401(k) contributions, there are only so many dollars available out of a paycheck. The order of priority is different for each person based on their personal tax situation, time frame at Nike, and plans for the future. We believe that the best way to determine the priority of one plan over another is through financial planning projections. Through the financial planning process, we take your financial considerations today and project them into the future. While this does not predict the future, it does allow you to measure the impact of each savings option and find the optimal course of action.

Solution to Cash-Flow Problem

A potential solution to the cash-flow challenge of participating in the Mega Backdoor Roth 401(k) contributions is to repurpose other funds. Available options that we have identified include existing after-tax accounts like Individual, Joint or Trust investment accounts, extra cash in the bank, or cash that you have from selling and diversifying out of Nike RSUs, ESPP, or Stock Options. You can use these accounts to supplement your cash flow while the Mega Backdoor Roth contributions are coming out of your paycheck.

Lower Your Tax Burden

While this strategy may not make sense for every Nike employee, it is a unique opportunity to get significant dollars into a Roth account that might not otherwise be available. Whether or not income taxes actually do increase in the future, the Nike Mega Backdoor Roth 401(k) is a very effective way to lower your long-term tax burden and should be considered as part of your financial plan.

If you want to know more about how to take advantage of the Nike Mega Backdoor 401(k), please get in touch.

You can schedule time with our team on Calendly, or e-mail us at nike@humanvesting.com.

*Assumes first Roth contribution made at least 5 years before withdrawal and withdrawals occur after age 59½.