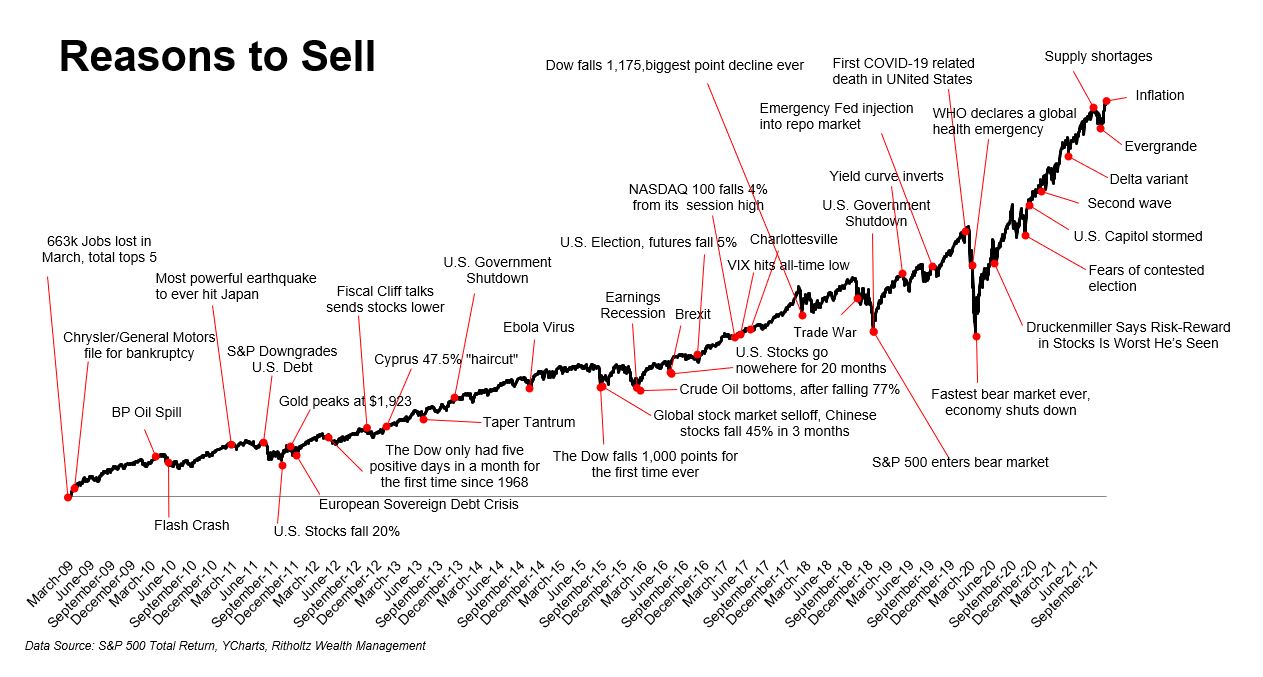

We’re all familiar with the risk-reward tradeoff: Do I risk injury to compete in a sport I love and feel fulfilled by? Do I risk leaving a stable job to pursue a career that excites me? It’s not surprising that this everyday phenomenon is also very present in our investment portfolios.

For example, there are three asset classes that an investor typically includes in their portfolio: cash, bonds, and stocks. Of the three, stocks can generate the greatest return but also merit the highest risk. On the other hand, a risk-free investment guarantees a future return with essentially no possibility of loss. An example of a risk-free investment is US Treasury bills, as they are backed by the full faith and credit of the US government. If investors are taking on more risk by investing in stocks, they want to know their efforts are worth it. Enter the equity risk premium.

Understanding the Equity Risk Premium

The equity risk premium measures how much more an investor may receive in returns when investing in stocks versus a risk-free investment like T-bills. Basically, it puts a number to the term, “the higher the risk, the higher the reward”.

As we’ve previously written, the fear of financial loss causes many investors to be overly cautious about their investments. ”Myopic loss aversion” is when focusing on avoiding short-term losses in equities leads to poor long-term allocation decisions. Incorporating bonds into your investment portfolio can serve as a stabilizer, reducing the payback period to see your portfolio recover from downturns. Many investors own some combination of stocks and bonds to ensure the risk-reward tradeoff is an acceptable range for them, either emotionally or financially (or both). Because of the fear of loss, many investors either avoid or under-weigh equities. How significant is the difference between owning stocks (highest risk), bonds (lower risk), or cash (no risk)?

Risks associated with investing in Stocks

So, why do those who invest in stocks generally receive a greater return? Because of the greater risk they take on by doing so, such as:

Unpredictability: Stocks do not offer fixed payments at specific intervals like bonds.

When an investor buys a bond, they are essentially lending money to a company or a government (see our Bonds 101 blog for a primer on bond basics). Like any loan, bonds have terms outlining specific payment amounts and dates. These payments, known as coupons or interest, are obligatory, with insolvency being the only reason for non-payment.

Conversely, stocks represent ownership in a company and entail greater uncertainty. Returns for stock investors can come in the form of dividends distributed by the company or by selling shares at a higher price in the future. Unlike bond payments, dividends are not mandatory and can be suspended unexpectedly, as seen during the onset of the COVID-19 pandemic. Additionally, the growth of dividends may not meet expectations, even for well-established companies commonly known as “blue chip” stocks (such as Coca-Cola, McDonalds, or Microsoft). Even large and stable companies face challenges that can cause fluctuations in their stock prices. Due to the unpredictability of stock payouts in terms of amount and timing, investing in stocks is inherently riskier and more volatile. As a result, investors demand higher returns from equities as compensation for bearing this additional risk.

Risk of Total Loss: Stockholders can see their investment go to zero more easily than bond investors.

Over the last thirty years, bondholders have frequently recouped 40% or more of their initial investment during bankruptcies, although exact recovery rates can vary[1]. In contrast, equity owners seldom receive any compensation in bankruptcy. The harsh reality is that most companies fail in the long term, and many of these companies made interest payments on bonds throughout their existence, while equity investors ultimately see their investments become worthless. Regardless of whether you’re investing in stocks or bonds, owning a broad index fund provides essential diversification. Owning a basket of companies ensures that even if one fails, the other companies that continue to grow offset your losses so you’re never experiencing a complete wipeout.

The Equity Premium at Play Can Sometimes be a Jackpot

First, a quick note: All return figures mentioned below are based on real returns, or returns after adjusting for inflation. Real returns are the most accurate comparison across different asset classes, reflecting changes in purchasing power over time. Although nominal returns are widely used in the financial world unless otherwise specified, they do not account for inflation and are therefore less accurate in this example. All returns are based on rolling 12-month periods, meaning this is the return if you held the investment for 12 months.

Table 1 - Real returns, rolling 12 month periods - (1926-2023, adjusted for inflation)[2]

When we look at the real returns for the last 97 years between cash, bonds, and equities, it’s clear stocks deliver the highest returns, albeit with the most downside risk. Cash is undeniably the safest asset class but struggles to outpace inflation. Bonds tend to be closer to cash than equities in terms of their risk-return profile.

The Long-Term Power of the Equity Premium for an Investor

While stocks undoubtedly offer the highest returns, it’s essential to grasp their long-term value to investors. To demonstrate this, let’s outline a hypothetical scenario:

Assume three investors each save $5K annually for 40 years for retirement for a total contribution of $200K per investor.

We’ll assume each investor owns only a single asset class (cash, bonds, or stocks) for all 40 years of saving.

We’ll use the real return averages from Table 1 for each asset class.

We’ll utilize the commonly cited 4% annual withdrawal rate[3] for retirees to determine how much income the portfolio provides in retirement annually.

Table 2 – Portfolio values assuming real returns

The difference in portfolio value, and resulting income possible in retirement, is significant. A pure equity investor ends up with nearly six times the spending power of a pure bond investor after 40 years.

While equity market volatility can be unsettling, exposure to equities can significantly reduce the amount of savings required to achieve your financial goals such as funding retirement. It’s critical to ensure your equity allocation is sufficient to facilitate asset growth yet small enough to prevent panic during market downturns. Striking this balance depends on your emotional risk tolerance and financial capacity for risk.

Determining the optimal equity and bond allocation requires careful consideration of factors such as taxes, time horizon, and liquidity needs. If you are seeking guidance in navigating this complex process, please reach out to us at 503-905-3100, or email hi@humaninvesting.com to start the conversation.

Sources

[1] https://www.spglobal.com/ratings/en/research/articles/231215-default-transition-and-recovery-u-s-recovery-study-loan-recoveries-persist-below-their-trend-12947167

[2] These returns are based on an index, do not represent actual investment results, and are not guarantees of future results.

Data based on rolling 12 month returns, with monthly return intervals.

Equity returns utilize the Ibbotson SBBI Large-Cap Stocks Total Return for Jan 1926 to Sep 1989 (data courtesy of CFA Institute), and S&P 500 TR for Oct 1989 to Dec 2023 (data courtesy of YCharts).

Bond returns utilize the Ibbotson SBBI US Intermediate Term Government Bonds Total Return for Jan 1926 to Apr 1996 (CFA Institute), and Bloomberg US Aggregate for May 1996 to Dec 2023 (YCharts).

Cash returns utilize the Ibbotson SBBI US (30-Day) Treasury Bills for Jan 1926 to May 1997 (CFA Institute), and Bloomberg US Treasury Bills 1-3 Month for Jun 1997 to Dec 2023 (YCharts).

Inflation rates for calculating real returns are based on the Ibbotson SBBI inflation for Jan 1926 to Jan 1947 (CFA Institute), and the Consumer Price Index (CPI) for Feb 1947 to Dec 2023 (YCharts).

[3] https://www.financialplanningassociation.org/sites/default/files/2021-04/MAR04%20Determining%20Withdrawal%20Rates%20Using%20Historical%20Data.pdf

{kind=link}