“Assuming AI doesn’t take my job first.” We’ve heard some version of that line from clients all year, almost always delivered with a nervous laugh. But behind the humor sits a question a lot of people are wrestling with right now.

Every meaningful shift in technology brings a mix of optimism and concern, and artificial intelligence is no different. For some, this is still a conversation about what might happen. For others, it has already shown up in tangible ways, whether your role has changed, been eliminated, or you're watching your industry transform in real time.

If that's where you are, the uncertainty isn't theoretical, and it isn't just financial. Work is tied to identity, routine, and a sense of progress, which makes disruption especially hard to process. And even if nothing has changed for you yet, it's difficult to ignore the possibility that it could.

Your Most Important Asset

For most people in the accumulation phase of life, the most important asset isn't a number in your portfolio: it's your ability to earn income over the next decade or more. When that ability feels less certain, everything connected to it can feel less stable.

When that uncertainty sets in, the natural instinct is to try to predict what happens next: Should I pivot? Is this temporary? Am I already behind? It's understandable, but what if the path ahead is too uncertain to plan around with confidence?

A more useful shift is to move from prediction to preparation. Rather than guessing the outcome, focus more on understanding how to remain steady across a range of possibilities.

Start With What You Can See

Financial stress often grows in the space between what's happening and what's understood. Not knowing how long savings will last can feel heavier than the actual number, and not knowing which expenses are fixed and which are flexible can make every decision feel harder than it needs to be.

The starting point is visibility. When the future feels undefined, the mind fills in the gaps (usually with worst-case scenarios). Taking even small steps to map the situation eases that pressure, because it turns something vague into something concrete. The numbers don't have to change; they just have to be visible.

In practice, that often starts with mapping your monthly spending in simple terms. What's essential? What's adjustable? A mortgage and insurance premiums are fixed, but a planned trip or a streaming subscription can flex if they need to. This isn't about building a perfect budget. It's about seeing your situation clearly enough to make decisions from a place of information rather than panic.

From there, structured planning does the rest. Turning a broad concern into a set of defined scenarios — What if my income drops 20%? What if I'm out of work for six months? — makes it possible to act with intention, even when the future stays uncertain. A plan that only works when everything goes right tends to feel fragile. Building in room for strain is what makes it hold up.

Margin Changes the Experience

Two households can face the same disruption and experience it very differently. What separates those experiences is often margin.

Cash doesn't eliminate risk, but it creates time. Time is what makes good decisions possible. With room to breathe, you can weigh options, wait out a market, take the right job instead of the first one. Without it, choices narrow and decisions become reactive instead of intentional.

The most useful way to measure margin is through the lens of time: how many months of essential expenses could I cover if my income changed? The number doesn't need to be perfect, but it gives you a runway. If margin already exists, the goal is to protect it. If it doesn't, the goal is to begin restoring it gradually as circumstances allow.

Some households add a second layer of flexibility by putting a line of credit in place while income is stable. A home equity line of credit (HELOC) is a common example. The purpose isn't to rely on it; it's to have access to it if needed. These options are far easier to secure before they're necessary, and much harder to obtain once income has already changed.

While this example is not specifically about AI disruption, it illustrates the broader value of financial flexibility when circumstances change unexpectedly. One family we worked with ran into this while moving between homes. They found the right next home before their current home had sold, creating a temporary cash gap that their savings alone couldn’t comfortably cover. Because they had established a HELOC while their income and balance sheet were still strong, they were able to bridge the timing difference without rushing the sale of their old home or liquidating investments in a way that would have created an unnecessary tax bill. Once the previous home sold, the line was paid back down. What the HELOC provided was time and the flexibility to make decisions from a position of stability instead of pressure.

Margin doesn't stop the disruption, but it shapes how you respond to it.

Optimizing Your Plan Has a Ceiling

During stable periods, optimization feels like the natural move. There are opportunities everywhere to maximize tax efficiencies, increase savings, and align decisions around long-term growth. Each move is prudent on its own. But the more tightly a plan is optimized, the less room it leaves to adjust when something changes.

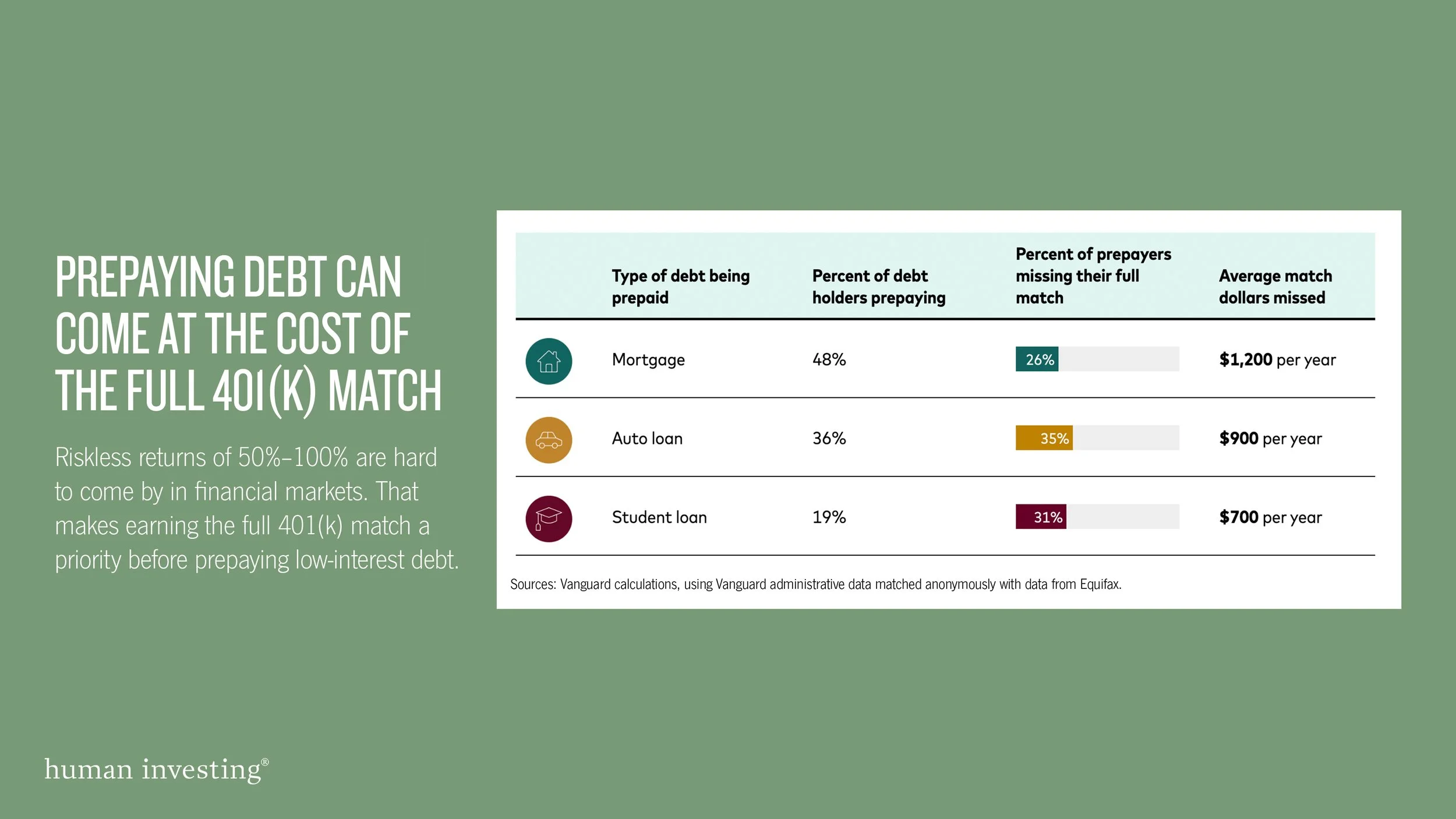

Retirement accounts illustrate the tension. They're powerful tools for building wealth, but they're built with constraints and hard to access when you need the money now. Assets that remain accessible before traditional retirement age may be less efficient by the numbers, but they offer something the optimized version can't: room to adjust.

The same pattern shows up in spending. As income rises, fixed commitments tend to rise alongside it. Bigger payments rarely feel restrictive in the moment, but when income changes or priorities shift, they can quickly reduce your ability to adjust.

Debt works similarly. Paying down a smaller obligation like a car loan creates real breathing room. Aggressively paying down a mortgage may improve the long-term math, but it locks money into your house that you can't easily get back if you need it.

Optimization assumes the future will look like the present, and flexibility assumes it might not. That's the difference between a plan that holds and a plan that breaks.

Another Form of Resilience

Visibility, margin, and flexibility are forms of resilience. There's another, less visible but increasingly important: what AI can’t replicate.

AI will keep reshaping how work gets done. It can already draft, analyze, and model at remarkable speed, and it will only get better. But the people who become most valuable (employees) won’t simply be the ones who know how to use AI. They’ll be the ones others trust when the stakes are high.

That kind of trust, the trust built when people share what's at stake, is what makes teams hold together when disruption hits. It's earned by showing up, by working through uncertainty together, by taking responsibility when outcomes aren't guaranteed.

AI can accelerate technical work, but it can’t replicate character, judgment, emotional steadiness, or genuine trust. In many ways, the rise of AI may make those qualities more valuable, not less. Used well, AI tends to amplify the people who already do good work, not replace them.

Create Your Adaptive Advantage

Preparing for uncertainty is less about reacting to every new development and more about maintaining a structure you can trust. In our experience, the people who navigate disruption well rarely anticipated every change. They took the time to understand their situation and made calculated adjustments along the way.

Alongside that structure, earning ability is something you can develop, not just protect. Staying current in your field, strengthening professional relationships, and gradually expanding into adjacent areas where your experience still applies all compound over time, even when the progress is hard to see in the moment.

If you're unsure where to begin, start small: understand your numbers, identify where you have flexibility, and take one step to strengthen your position. Clarity tends to build from there.

Preparation doesn't remove uncertainty, but it can keep uncertainty from making your decisions for you. In periods like this, that steadiness tends to matter more than most people expect.