Looking to go on a “once in a lifetime” trip to Fiji? Remodel your kitchen? Buy a new car? If your employer plan allows it, you may be tempted to take out a loan from your 401(k) to help fund that major expense.

Before you do, let’s talk through what a 401k loan looks like today and why borrowing from your future self can cost far more than you expect.

The Details

If your 401(k) plan allows loans, you can technically borrow up to $50,000 or 50% of your owned retirement savings (vested balance), whichever is less. There’s no credit check, and repayments are automatically taken from your paycheck.

For 2025, the interest rate on a 401k loan is roughly 9.50% (Rate of Prime + 1%). That’s a high rate for borrowing from yourself, and it can add up quickly. While the interest you pay goes back into your account, it’s still your retirement money being used, which could slow long-term growth.

Even though it’s allowed, taking a loan from your 401(k) isn’t usually recommended: about 1 in 5 people with a 401(k) have a loan at any given time, but doing so can put your future financial security at risk.

The Dangerous Reality

Still sounds pretty good, right? Well… not so fast.

A 401(k) loan can come at a real cost and not just the money you pull out today. It’s the potential long-term growth and retirement dollars you lose out on by stepping out of the market and halting contributions.

Here’s what you need to understand:

You lose tax-advantaged growth

Loan repayments are made with after-tax dollars. Then you’ll likely pay tax again when withdrawing the funds in retirement. That double-tax effect makes the math harder to win.

You could face a tax bill and penalty if you change jobs

If you leave your employer before the loan is repaid, the remaining balance typically must be paid back by tax filing time. If not, the balance becomes taxable and if you are under 59½, you may face a 10% early withdrawal penalty.

Stopping contributions

Many borrowers pause contributions while repaying the loan. If your plan gives an employer match, that means you may miss out on free money.

Dollars stop compounding

The money you borrow no longer participates in the market. In periods of growth, missing out on compounding has long-term consequences.

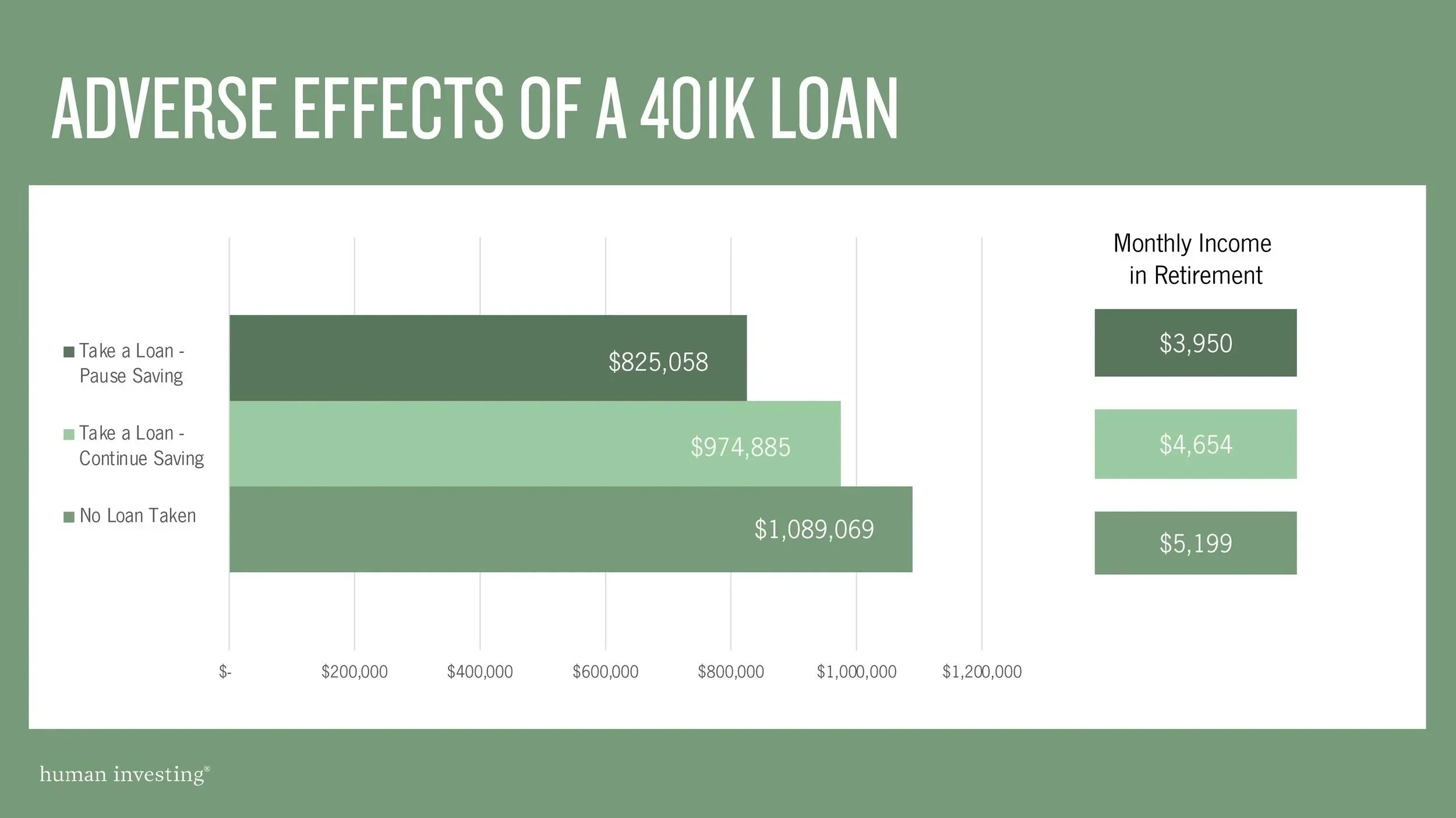

A Real-Life Example

Say you make $75,000 a year and want to borrow $15,000 from your 401(k) to fund a big trip or home project. To make the loan payments easier, you pause your 401(k) contributions while you pay it back.

Let’s also assume you already have $50,000 saved in your 401(k) when you take this loan.

Here’s what happens:

You normally save 7% of your pay ($5,250/year)

Your employer matches another 3% ($2,250/year)

By stopping contributions for three years, you miss:

$15,750 you would have put in

$6,750 your employer would have matched

That’s $22,500 total that never gets invested.

Now let’s look at the long-term impact.